+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Conductive Polymer Tantalum Solid Capacitor Market to Reach $962 Million by 2030, Growing at 6.3% CAGR

Global Conductive Polymer Tantalum Solid Capacitor Market to Reach $962 Million by 2030, Growing at 6.3% CAGR

Wednesday,08 Jul,2026

Conductive Polymer Tantalum Solid Capacitor: Definition and Principles

Conductive polymer tantalum solid capacitors are a type of electrolytic capacitor that utilizes a tantalum anode (made from tantalum powder sintered into a porous pellet) and a conductive polymer cathode (typically PEDOT:PSS — poly(3,4-ethylenedioxythiophene) polystyrene sulfonate, or similar conductive polymers) as the solid electrolyte, replacing the traditional manganese dioxide (MnO₂) or liquid electrolyte in conventional tantalum capacitors. This construction enables very small size, high capacitance in a small and low-profile form factor, low equivalent series resistance (ESR) , stable performance over time, and a benign failure mode under recommended use conditions.

Key features and advantages:

-

Very small size and high volumetric efficiency: Conductive polymer tantalum solid capacitors offer high capacitance values in compact, low-profile packages (down to 0402 case sizes), making them ideal for space-constrained applications.

-

Low ESR: Significantly lower ESR than conventional tantalum capacitors, enabling high ripple current handling and efficient power delivery in demanding applications.

-

Stable capacitance and ESR over time: Unlike liquid electrolyte capacitors (which can dry out), conductive polymer capacitors exhibit excellent aging stability.

-

Benign failure mode: Under recommended use conditions, conductive polymer tantalum capacitors fail open-circuit or short-circuit with low risk of ignition or catastrophic failure, enhancing system safety.

-

Wide temperature range: Typically operate from -55°C to +125°C, suitable for industrial and automotive applications.

-

High ripple current capability: Can handle higher ripple currents than equivalent MnO₂-based tantalum capacitors.

Key parameters:

-

Capacitance range: Typically 1 µF to 1,000+ µF (depending on voltage rating and case size).

-

Voltage rating: 2.5 V to 50 V (higher ratings available for specialized applications).

-

ESR: As low as 5–10 mΩ for high-performance grades.

-

Operating temperature: -55°C to +125°C (derating applies at higher temperatures).

Product type segmentation (by form factor):

-

Chip Capacitors (largest segment, >80% share): Surface-mount device (SMD) capacitors designed for automated PCB assembly. Chip capacitors dominate the market due to their suitability for high-density electronic assembly, compatibility with standard pick-and-place equipment, and broad adoption in consumer electronics, industrial, and automotive applications.

-

Leaded / Radial Leaded Capacitors: Through-hole capacitors with axial or radial leads, used in legacy applications and some industrial and aerospace designs.

Conductive Polymer Tantalum Solid Capacitor Market Summary

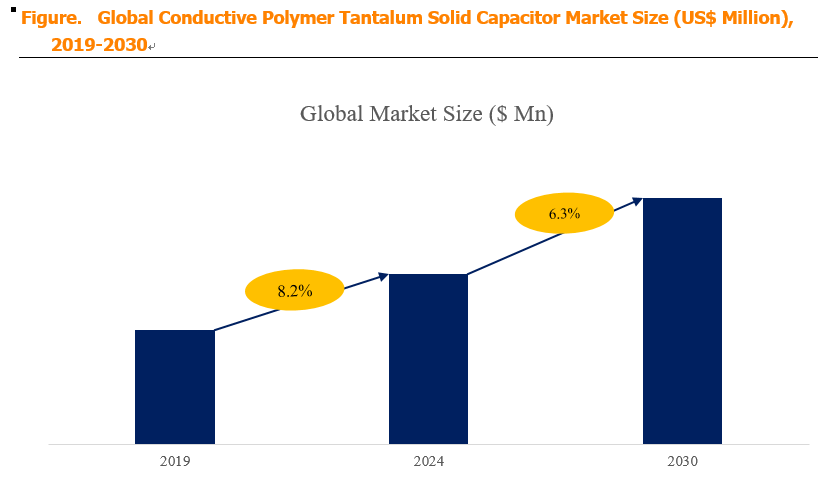

According to a new market research report published by Market Monitor Global, the global Conductive Polymer Tantalum Solid Capacitor market was valued at USD 632 million in 2023 and is projected to grow to USD 962 million by 2030, at a compound annual growth rate (CAGR) of 6.3% during the forecast period. This steady growth is driven by the increasing demand for compact, high-performance capacitors in portable electronics, electric vehicles (EVs), automotive electronics, industrial applications, and the proliferation of IoT devices.

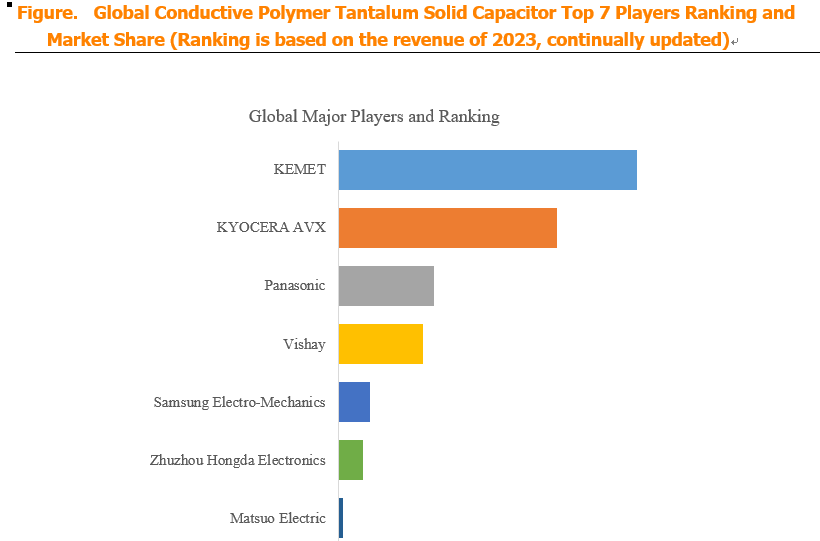

Market Monitor Global's analysis indicates that the global key manufacturers of Conductive Polymer Tantalum Solid Capacitors include KEMET (USA — a Yageo company), KYOCERA AVX (USA/Japan), Panasonic (Japan), and Vishay (USA). In 2023, the global top three players collectively accounted for approximately 77% of total revenue, indicating an extremely concentrated market dominated by a few established players with deep expertise in tantalum capacitor technology. KEMET and KYOCERA AVX are the market leaders, offering broad portfolios of conductive polymer tantalum capacitors. Panasonic is a strong competitor, particularly in the consumer electronics and automotive segments. Vishay is a significant player, with a focus on industrial, military, and aerospace applications.

In terms of product type, Chip Capacitors are the largest segment, accounting for over 80% of the market. Surface-mount chip capacitors dominate due to their compatibility with automated PCB assembly, small footprint, and suitability for modern, high-density electronic devices.

Regarding application, Consumer Electronics is the largest segment, accounting for 43% of the market. Key applications include:

-

Smartphones: For power management, decoupling, and filtering in compact designs.

-

Tablets and laptops: For CPU/GPU power delivery and energy storage.

-

Wearables (smartwatches, fitness trackers): For compact power management and energy storage.

-

SSDs (Solid State Drives): For power decoupling and energy storage.

-

Digital cameras, gaming consoles, and other portable devices.

The Automotive segment (including EVs), Industrial (power supplies, motor drives, factory automation), Medical, and Aerospace/Defense segments account for the remainder, with automotive being the fastest-growing segment.

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by the concentration of consumer electronics manufacturing (China, Taiwan, South Korea), the rapid growth of the EV market in China and South Korea, and the expanding industrial sector. North America and Europe are mature markets, driven by automotive, industrial, aerospace, and military applications.

Conductive Polymer Tantalum Solid Capacitor Market Dynamics

Market Drivers:

-

D1: Growth in portable electronics and electric vehicles (EVs) – The proliferation of portable electronics (smartphones, tablets, laptops, wearables) and the rapid adoption of electric vehicles are key demand drivers:

-

Smartphones and tablets: Require high-capacitance, low-ESR, compact capacitors for power management, decoupling, and filtering.

-

EVs: Use conductive polymer tantalum capacitors for:

-

Inverters and converters: For DC/DC conversion and filtering.

-

Battery management systems (BMS): For power management and sensing.

-

On-board chargers (OBCs): For power conditioning.

-

ADAS (Advanced Driver Assistance Systems): For power supply filtering and decoupling.

As EV adoption accelerates globally, demand for automotive-grade conductive polymer tantalum capacitors increases.

-

-

-

D2: Low ESR and high capacitance driving performance advantages – Conductive polymer tantalum capacitors offer:

-

Low ESR: Enables efficient power delivery, reduced power losses, and improved transient response.

-

High capacitance: Provides effective decoupling and energy storage in small packages.

-

High ripple current capability: Suitable for high-frequency, high-current applications.

-

Stable performance over time: Excellent aging stability compared to liquid electrolyte capacitors.

These performance advantages make them the preferred choice for demanding applications in automotive, industrial, and consumer electronics.

-

-

D3: Proliferation of Internet of Things (IoT) devices – The rapid growth of IoT devices (sensors, smart home devices, wearables, industrial IoT) drives demand for compact, efficient, and reliable capacitors. Key requirements:

-

Small form factor: For integration into compact, battery-powered devices.

-

Low power consumption: Compatible with energy-efficient designs.

-

Long operational life: Suitable for devices intended for years of operation.

-

Wide operating temperature: For outdoor and industrial IoT applications.

-

-

D4: Shift toward high-reliability automotive and industrial applications – Automotive and industrial applications increasingly require:

-

High reliability: Long service life, low failure rates, and benign failure modes.

-

High temperature capability: Operating temperatures up to 125°C and beyond.

-

Vibration and shock resistance: Essential for automotive and industrial environments.

Conductive polymer tantalum capacitors meet these requirements, making them a preferred choice in these sectors.

-

Market Restraints:

-

R1: Raw material price volatility and supply chain risks – Tantalum (the primary raw material for the anode) is:

-

Price-volatile: Prices are influenced by global supply-demand balances, mining disruptions, and geopolitical factors (tantalum is mined in several regions, including Australia, Brazil, the Democratic Republic of Congo, and others).

-

Subject to supply chain risks: Conflict minerals regulations (e.g., Dodd-Frank Act Section 1502) require sourcing from conflict-free suppliers, which can add compliance costs and limit supply.

-

Dependent on recycling: A significant proportion of tantalum supply comes from recycling, but recycling rates and prices are also subject to volatility.

Tantalum price fluctuations directly impact capacitor production costs and profit margins.

-

-

R2: Competition from alternative capacitor technologies – Conductive polymer tantalum capacitors compete with:

-

Ceramic capacitors (MLCCs): Offer lower cost, smaller sizes, and excellent high-frequency performance. However, they have lower capacitance values and are more susceptible to piezoelectric effects (microphonics).

-

Aluminum electrolytic capacitors: Lower cost but larger size, higher ESR, and shorter lifespan.

-

Conductive polymer aluminum capacitors: Offer low ESR and high reliability, but may have lower capacitance or higher cost.

-

Tantalum capacitors with MnO₂ electrolyte: Lower cost but higher ESR and less benign failure mode.

For cost-sensitive applications, ceramic or aluminum electrolytic capacitors may be preferred.

-

-

R3: High manufacturing complexity and quality requirements – Conductive polymer tantalum capacitors require:

-

Precise tantalum powder processing: Sintering to form porous anodes with controlled porosity.

-

Precise anodization: Forming a high-quality tantalum oxide (Ta₂O₅) dielectric layer.

-

Polymer deposition: Uniform and defect-free conductive polymer coating.

-

High-reliability testing: Extensive screening (electrical, thermal, environmental) to ensure reliability.

Manufacturing complexity and stringent quality requirements create high barriers to entry and limit the number of qualified suppliers.

-

Market Opportunities:

-

O1: Development of higher-voltage and higher-reliability grades – There is growing demand for:

-

Higher voltage ratings (up to 50 V and beyond): For automotive, industrial, and power supply applications.

-

Extended temperature ranges (up to 150°C+): For automotive under-hood and industrial high-temperature environments.

-

AEC-Q200 qualification: Automotive-grade qualification, increasingly required by automotive OEMs and tier-1 suppliers.

-

Military/aerospace specifications: High-reliability grades with extensive testing and lot traceability.

Manufacturers that develop and qualify higher-voltage and higher-reliability products can capture premium segments.

-

-

O2: Expansion into automotive electronics and EV applications – Automotive electronics is the fastest-growing segment. Opportunities include:

-

ADAS: For power supply filtering, decoupling, and energy storage.

-

Inverters and converters: For DC/DC conversion and power conditioning.

-

BMS: For power management and sensing.

-

On-board chargers: For power filtering and decoupling.

-

LED lighting: For power management and filtering.

As automotive content continues to increase (per-vehicle capacitor content is growing), the addressable market expands.

-

-

O3: Development of smaller case sizes and higher capacitance density – Consumer electronics and wearables demand ever-smaller components. Opportunities include:

-

Smaller case sizes: Down to 0402 (1.0 mm × 0.5 mm) and smaller.

-

Higher capacitance in smaller packages: Enabling integration into space-constrained devices.

-

Lower profile capacitors: For ultra-thin devices.

-

Higher ripple current capability: For power-dense applications.

Manufacturers that push the boundaries of miniaturization and capacitance density can gain market share in consumer electronics.

-

-

O4: Integration into IoT and connected devices – The proliferation of IoT devices (sensors, wearables, smart home, industrial IoT) creates demand for:

-

Ultra-small capacitors: For compact sensor nodes and wearable devices.

-

Low leakage current: For battery-powered devices requiring extended battery life.

-

High reliability: For devices in harsh or outdoor environments.

-

Cost-effective solutions: For high-volume, cost-sensitive IoT applications.

-

-

O5: Strategic partnerships and supply chain resilience – Given the concentrated nature of the market and supply chain risks for tantalum, there are opportunities for:

-

Long-term supply agreements: With tantalum powder suppliers to ensure stable supply and predictable pricing.

-

Investment in tantalum recycling: To reduce dependence on primary tantalum mining and mitigate price volatility.

-

Dual-sourcing of raw materials: To reduce supply chain risk.

-

Regional manufacturing expansion: To serve growing regional markets (particularly Asia-Pacific).

-

`{IZ}V5{D~CF~[X5~6J`IC.png)

Industry Trends:

-

Dominance of chip capacitors: Chip capacitors (>80% share) dominate the market due to their compatibility with automated PCB assembly and high-density designs.

-

High market concentration: Top three players account for ~77% of the market, reflecting high technical barriers, supply chain integration, and strong customer relationships.

-

Consumer electronics as largest application: Consumer electronics (43% share) is the largest application segment, driven by smartphones, tablets, laptops, and wearables.

-

Fast-growing automotive sector: Automotive (particularly EV) is the fastest-growing application, driven by increasing electronic content per vehicle and high demand for high-reliability, high-temperature capacitors.

-

Pressure from alternative capacitor technologies: Ceramic capacitors (MLCCs) and aluminum electrolytic capacitors compete on cost and performance, limiting market growth in some segments.

-

Supply chain and raw material risks: Tantalum supply is concentrated and subject to price volatility, conflict minerals regulations, and geopolitical risks.

78WSHPD76.png)

Industry Structure and Competitive Dynamics

The global Conductive Polymer Tantalum Solid Capacitor market is characterized by an extremely concentrated competitive landscape:

-

Market leaders (KEMET, KYOCERA AVX, Panasonic): These three players account for ~77% of global revenue. Their advantages include:

-

Deep tantalum expertise: Decades of experience in tantalum metallurgy, capacitor design, and manufacturing.

-

Vertical integration: Control over tantalum powder sourcing, sintering, anodization, polymer deposition, and packaging.

-

Broad product portfolios: Covering a wide range of capacitance, voltage, case sizes, and application grades.

-

Strong customer relationships: Long-term partnerships with major OEMs in consumer electronics, automotive, and industrial sectors.

-

AEC-Q200 and MIL-spec qualifications: Products qualified for automotive, military, and aerospace applications.

-

-

Other significant players (Vishay, others): Vishay offers a broad range of tantalum capacitors, serving industrial, military, and aerospace markets. Other players include smaller specialist manufacturers and regional suppliers.

Key success factors in this market:

-

Raw material access and cost management: Secure supply of tantalum, polymer materials, and other critical components.

-

Manufacturing scale and efficiency: High-volume, low-cost production with high yields.

-

Product innovation: Developing smaller case sizes, higher capacitance, lower ESR, and higher voltage ratings.

-

Quality and reliability: Meeting AEC-Q200, military, and aerospace reliability requirements.

-

Regulatory compliance: Managing conflict minerals regulations, REACH, RoHS, and other environmental regulations.

-

Customer relationships: Long-term partnerships with major OEMs and EMS providers.