+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

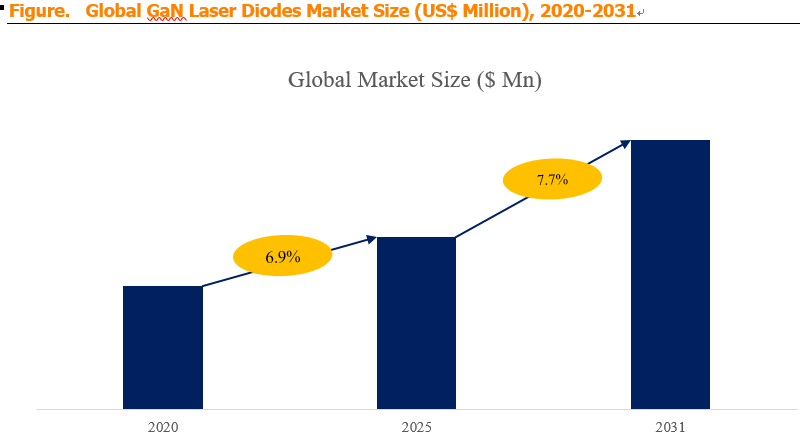

Log In Global GaN Laser Diodes Market to Reach $1.76 Billion by 2031, Growing at 7.71% CAGR

Wednesday,08 Jul,2026

GaN Laser Diodes: Definition and Principles

GaN Laser Diodes are optoelectronic devices based on the third-generation semiconductor material gallium nitride (GaN) . They generate laser light through electron-hole recombination, emitting primarily short-wavelength lasers such as violet (405 nm) , blue (440–460 nm) , and green (520–530 nm) light. GaN laser diodes offer distinct advantages — including high efficiency, high power, wide wavelength range, compact size, and long lifetime — making them ideal for applications ranging from optical displays and optical storage to industrial processing, medical devices, automotive lighting, and consumer electronics.

Key technical characteristics:

-

Wavelength range: GaN laser diodes typically operate in the UV–visible–green (380–530 nm) spectrum, which is shorter than the near-infrared (780–1,550 nm) wavelengths of traditional InGaAsP/InP lasers. The ability to emit in the blue and green regions is particularly valuable for display and projection applications.

-

High efficiency: GaN lasers offer superior electrical-to-optical conversion efficiency compared to older technologies.

-

High power: Capable of delivering high output power (from milliwatts to several watts) for demanding applications like laser processing and projection.

-

Compact size: Small footprint enables integration into portable devices, head-mounted displays, and automotive lighting systems.

-

Long lifetime: GaN lasers demonstrate excellent reliability, with lifetimes exceeding 10,000–20,000 hours in many applications.

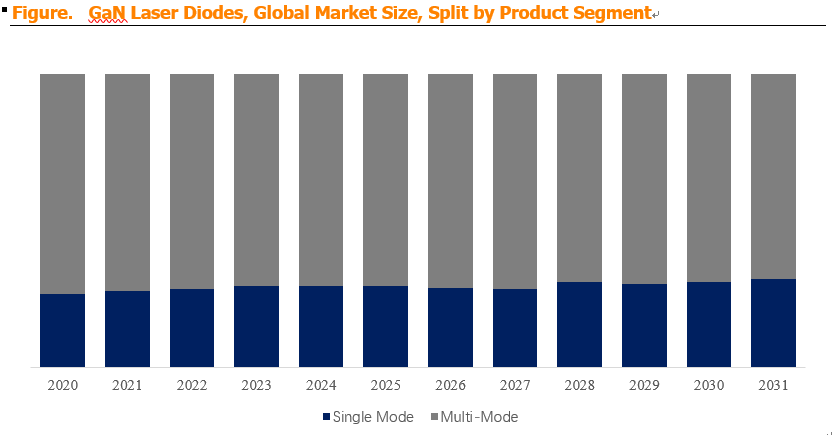

Product type segmentation (by lasing mode):

-

Multi-Mode (largest segment, 72.1% share): Multi-mode GaN laser diodes support multiple transverse modes, delivering high power (typically >500 mW to several watts) . They are used in projectors, laser displays, industrial processing (cutting, welding, marking), and medical devices where high power is prioritized over beam quality.

-

Single-Mode: Single-mode lasers produce a single transverse mode, providing high beam quality (M² < 1.3) and narrow spectral linewidth. They are used in applications requiring precise focusing and high spatial coherence, such as optical storage (Blu-ray), fiber coupling, biomedical sensing, metrology, and telecommunications.

GaN Laser Diodes Market Summary

According to a new market research report published by Market Monitor Global, the global GaN Laser Diodes market was valued at US 1,758.43 million by 2031, at a compound annual growth rate (CAGR) of 7.71% during the forecast period. This strong growth is driven by the expanding adoption of laser projection and display technologies, the proliferation of augmented reality (AR) and virtual reality (VR) devices, increasing demand for laser-based industrial processing, and the growing use of GaN lasers in automotive lighting and medical applications.

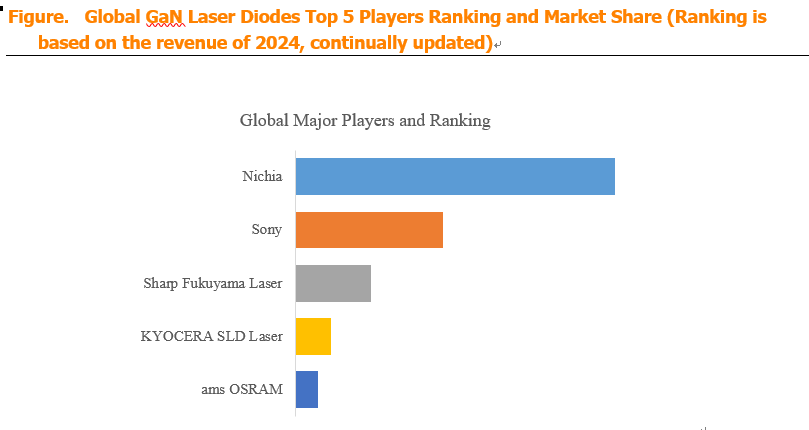

Market Monitor Global's analysis indicates that the global key manufacturers of GaN Laser Diodes include Nichia (Japan), Sony (Japan), Sharp Fukuyama Laser (Japan), KYOCERA SLD Laser (Japan/USA), and ams OSRAM (Austria/Germany). In 2024, the global top three players collectively accounted for approximately 85% of total revenue, indicating an extremely concentrated market dominated by Japanese and European manufacturers. Japanese companies (Nichia, Sony, Sharp) hold dominant positions in the blue-violet and blue laser markets, leveraging decades of expertise in GaN epitaxial growth and device fabrication. ams OSRAM (from the merger of ams and OSRAM) is a European powerhouse in visible laser diodes, particularly in green and blue lasers for automotive and industrial applications.

In terms of product type, Multi-Mode is the largest segment, holding a 72.1% share. Multi-mode devices dominate the market due to their higher output power and broad applicability in projection, display, and industrial processing. Single-Mode lasers account for the remainder, serving precision applications like optical storage, metrology, and biomedical sensing.

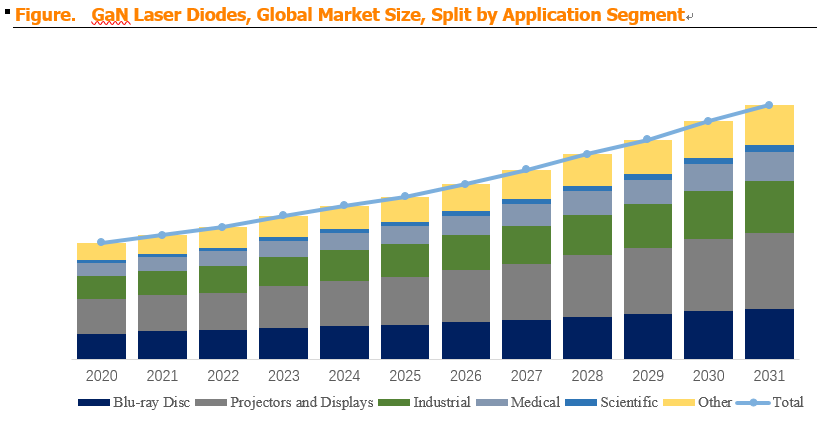

Regarding application, Projectors and Displays is the largest segment, accounting for 29.5% of the market. GaN laser diodes are used in laser projectors (for cinemas, home theaters, and professional AV), laser TV, and head-up displays (HUDs). Their superior brightness, color gamut, and energy efficiency make them an attractive alternative to traditional lamp-based projectors. Industrial Processing is the second-largest segment, driven by laser cutting, welding, marking, and additive manufacturing. Medical Devices (dermatology, surgery, diagnostics), Automotive Lighting (laser headlights), Optical Storage (Blu-ray), and Other applications (AR/VR, LiDAR, communications) account for the remainder.

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by Japan's leadership in GaN laser diode manufacturing (Nichia, Sony, Sharp), China's rapidly expanding display and consumer electronics industries, and South Korea's strong display sector. North America is a significant market, driven by demand for laser projectors, AR/VR devices, industrial processing, and automotive applications. Europe is a mature market, with strong demand from automotive (laser headlights), medical, and industrial applications.

GaN Laser Diodes Market Dynamics

Market Drivers:

-

D1: Growing demand for laser projection and display technologies – Laser projectors offer superior brightness, color gamut, and energy efficiency compared to traditional lamp-based projectors. GaN laser diodes are the key light source enabling these benefits. The growing adoption of laser projection in:

-

Cinemas (upgrading from xenon lamps to laser illumination).

-

Home theaters (premium laser TVs and projectors).

-

Professional AV (conference rooms, education, events).

-

Head-up displays (HUDs) in automotive.

-

Laser-based augmented reality (AR) and mixed reality (MR) headsets (emerging applications) is driving demand.

-

-

D2: Proliferation of AR/VR and wearable display devices – AR/VR headsets, smart glasses, and wearable displays increasingly use GaN laser diodes as light sources for retinal scanning, waveguide-based displays, and other optical architectures. The unique advantages of GaN lasers — small footprint, high efficiency, and direct modulation capability — make them ideal for these compact, power-sensitive devices.

-

D3: Expansion of industrial laser processing – GaN lasers (particularly green and blue wavelengths) are increasingly used in industrial processing applications:

-

Cutting and welding: Blue and green lasers offer superior absorption in copper and aluminum, enabling efficient welding and cutting of these materials.

-

Marking and engraving: High-precision marking of metals, plastics, and other materials.

-

Additive manufacturing: Laser-based 3D printing and powder bed fusion.

-

Laser cleaning: Removing coatings, rust, and contaminants.

-

-

D4: Growth in medical and aesthetic applications – GaN laser diodes are used in:

-

Dermatology: Skin rejuvenation, hair removal, and treatment of vascular lesions.

-

Ophthalmology: Retinal treatments and vision correction.

-

Surgery: Precision cutting and coagulation.

-

Diagnostics: Fluorescence spectroscopy, photodynamic therapy.

-

Market Challenges & Restraints:

-

R1: High material and epitaxial costs – GaN laser diodes are manufactured on GaN substrates or sapphire substrates (with GaN epitaxial layers). GaN substrates are expensive due to:

-

High production costs: Growing large-diameter, low-defect GaN single crystals is challenging and costly.

-

Limited supply: 90% of global GaN substrate production capacity is concentrated in a few Japanese companies (Sumitomo Electric, Mitsubishi Chemical). This creates supply chain risks and price volatility.

-

MOCVD equipment monopoly: Metal-organic chemical vapor deposition (MOCVD) equipment, essential for GaN epitaxial growth, is dominated by a few suppliers (Veeco, Aixtron), limiting capacity and increasing costs.

-

-

R2: Manufacturing complexity and defect control – GaN laser diode manufacturing faces core challenges:

-

Material defects: GaN epitaxial layers are prone to high dislocation densities, which degrade laser performance and lifetime. Reducing defects requires advanced growth techniques and optimization.

-

Thermal management: High-power GaN lasers generate significant heat, requiring efficient thermal management (packaging, heat sinking) to maintain performance and reliability.

-

Process complexity: Manufacturing GaN lasers involves multiple complex steps (epitaxy, etching, metallization, cleaving, facet coating, packaging), each with significant yield and cost implications.

-

-

R3: Geopolitical and trade uncertainties – Factors such as changes in trade policies, tariffs, and geopolitics have an adverse impact on industry development:

-

US bans on Chinese semiconductor equipment restrict China's ability to develop advanced GaN manufacturing capacity.

-

EU's Critical Raw Materials Directive may impose restrictions or require localization for certain critical materials.

-

US-China trade tensions create uncertainty in supply chains, export controls, and market access.

These uncertainties complicate investment decisions and can disrupt supply chains.

-

-

R4: Competition from alternative laser technologies – GaN laser diodes face competition from:

-

Diode-pumped solid-state (DPSS) lasers: Offering higher power and beam quality in some applications, but typically larger and more expensive.

-

Fiber lasers: Dominant in high-power industrial processing (cutting, welding).

-

CO₂ lasers: Still used for certain materials processing.

-

VCSELs (Vertical-Cavity Surface-Emitting Lasers): Competing in some consumer and sensing applications.

-

Market Opportunities:

-

O1: Expansion into automotive lighting (laser headlights) – Laser headlights offer superior brightness, range, and energy efficiency compared to LED headlights. Key advantages:

-

High brightness: Laser headlights can project light over 600+ meters, significantly improving nighttime visibility.

-

Compact design: Laser sources are small, enabling innovative headlight designs.

-

Intelligent lighting: Laser headlights can be dynamically steered (using beamforming) to avoid blinding oncoming traffic.

-

High efficiency: Laser headlights are more efficient than LED headlights in terms of lumens per watt.

As automotive manufacturers increasingly adopt laser headlights (e.g., BMW, Audi, Mercedes), demand for GaN laser diodes in this application will grow.

-

-

O2: Development of high-power green and blue lasers for industrial use – Green and blue lasers are increasingly important for:

-

Copper and aluminum welding: Blue and green lasers have better absorption in these metals than infrared lasers, enabling more efficient welding.

-

High-precision cutting: Green lasers offer finer beam quality for precision cutting.

-

Additive manufacturing: Laser-based 3D printing of metals and polymers.

-

Laser cleaning: Removing coatings, rust, and contaminants.

As industrial adoption increases, the demand for high-power multi-mode GaN lasers will grow.

-

-

O3: Growth of AR/VR and consumer electronics – GaN lasers are being adopted in:

-

AR/VR headsets: For retinal scanning, waveguide displays, and laser projection.

-

Smart glasses: Compact, low-power laser modules for wearable displays.

-

Consumer projectors: Portable, battery-powered laser projectors.

-

Laser lighting: In smartphones, wearables, and other consumer devices.

-

-

O4: Advanced manufacturing and automation – GaN lasers are used in:

-

Laser micro-machining: Drilling, cutting, and structuring of materials (glass, ceramics, metals).

-

Laser marking: High-contrast, permanent marking of components.

-

Laser structuring: Surface texturing and patterning.

-

Laser ablation: Removing layers from thin-film structures.

-

-

O5: Advances in GaN substrate technology and cost reduction – Ongoing R&D is focused on:

-

Lower-cost GaN substrates: Developing alternative growth techniques (e.g., HVPE, ammonothermal) to reduce substrate costs.

-

Larger-diameter GaN substrates: Reducing cost per device and enabling economies of scale.

-

Improved epitaxial quality: Reducing defect density and improving device performance.

-

Packaging innovation: Developing advanced packaging solutions (e.g., micro-optics, monolithic integration) to reduce cost and improve performance.

As these advances mature, the cost of GaN laser diodes will decrease, expanding their market potential.

-

Industry Structure and Competitive Dynamics

The global GaN Laser Diodes market is characterized by an extremely concentrated competitive landscape:

-

Japanese leaders (Nichia, Sony, Sharp): These companies dominate the blue-violet and blue laser segments, driven by their expertise in GaN epitaxy and device fabrication. They hold extensive patents and strong customer relationships in optical storage, projection, and display.

-

European leader (ams OSRAM): A dominant player in green lasers, automotive lighting, and industrial applications. The company's expertise in packaging, thermal management, and system integration differentiates it from Japanese competitors.

-

Niche players (KYOCERA SLD Laser): A subsidiary of KYOCERA, focusing on high-power and high-reliability GaN lasers for industrial, automotive, and defense applications.

Key success factors in this market:

-

Epitaxial growth expertise: Ability to grow high-quality GaN epitaxial layers with low defect density.

-

Device design and fabrication: Design of efficient laser structures, thermal management, and packaging.

-

Supply chain resilience: Secure access to GaN substrates, MOCVD equipment, and other key materials/equipment.

-

Customer relationships: Partnerships with display manufacturers, automotive OEMs, and industrial equipment producers.

-

Innovation: Continuous R&D to improve power, efficiency, and reduce costs.