+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global SCR Denitration Catalyst Market to Reach $2.26 Billion by 2030, Growing at 6.9% CAGR

Global SCR Denitration Catalyst Market to Reach $2.26 Billion by 2030, Growing at 6.9% CAGR

Monday,06 Jul,2026

SCR Denitration Catalyst: Definition and Principles

SCR (Selective Catalytic Reduction) Denitration Catalyst is a type of catalyst — typically based on titanium dioxide (TiO₂) as the primary support material, with vanadium pentoxide (V₂O₅) and tungsten trioxide (WO₃) or molybdenum trioxide (MoO₃) as active components — that promotes the selective reaction of reducing agents (usually ammonia (NH₃) or urea) with nitrogen oxides (NOₓ, primarily NO and NO₂) in flue gas at a controlled temperature range (typically 300–420°C), producing nitrogen (N₂) and water (H₂O) . This process effectively removes NOₓ from flue gas, reducing emissions of acid-rain precursors and ground-level ozone precursors.

Basic chemical reaction:

4 NO + 4 NH₃ + O₂ → 4 N₂ + 6 H₂O

2 NO₂ + 4 NH₃ + O₂ → 3 N₂ + 6 H₂O

NO + NO₂ + 2 NH₃ → 2 N₂ + 3 H₂O

The catalyst itself is not consumed in the reaction; it provides an active surface where the reactants (NOₓ, NH₃, O₂) adsorb, react, and desorb as products (N₂, H₂O). The catalyst's composition, pore structure, and surface area determine its activity (conversion efficiency), selectivity (minimizing unwanted side reactions, such as SO₂ oxidation to SO₃ or NH₃ slip), and durability (resistance to poisoning, fouling, and thermal degradation).

SCR is a mature, proven technology widely used in back-end processing (post-combustion) for DeNOₓ applications, and is the most common technology used for NOₓ control, particularly in the thermal power industry (coal-fired, gas-fired, and oil-fired power plants), as well as in cement production, iron and steel manufacturing, glass production, petrochemicals, marine engines, and other industrial processes.

Key catalyst types (by geometry/structure):

-

Honeycomb Catalyst (largest segment, 77.0% share): Extruded ceramic (TiO₂-based) monolith with thousands of parallel channels (square or triangular cross-section). Provides high surface area per unit volume, low pressure drop, and good mechanical strength. Widely used in large-scale applications (power plants, industrial boilers).

-

Plate Catalyst: Thin metal plates coated with catalyst material, arranged in parallel plates with gaps. Lower pressure drop, higher dust tolerance, and easier cleaning. Used in high-dust applications (e.g., coal-fired power plants with high particulate loading).

-

Corrugated Catalyst: Corrugated ceramic or metal sheets (with or without fiber reinforcement) providing moderate surface area and good mass transfer. Used in some industrial applications (cement, waste incineration).

YR{Y0(GVPCOU.png)

Key performance and design parameters:

-

DeNOₓ efficiency (NOₓ conversion rate): Typically 80-95% in modern SCR systems.

-

NH₃ slip (unreacted ammonia): Must be minimized (< 5 ppm) to prevent downstream ammonium bisulfate formation (which can foul air preheaters) and to meet regulatory limits.

-

SO₂ oxidation rate: Vanadium-based catalysts oxidize some SO₂ to SO₃, which can cause corrosion and ammonium bisulfate fouling. Catalyst formulations are optimized to minimize SO₂ oxidation.

-

Operating temperature window: Typically 300-420°C for high-activity catalysts; lower-temperature catalysts (for downstream placement) operate at 170-250°C.

-

Lifetime: 3-5 years for high-dust applications (coal-fired) to 5-8 years for low-dust or gas-fired applications; limited by mechanical erosion, chemical poisoning (arsenic, phosphorus, alkaline metals), and thermal aging.

SCR Denitration Catalyst Market Summary

According to a new market research report published by Market Monitor Global, the global SCR Denitration Catalyst market is projected to reach USD 2.26 billion by 2030, at a compound annual growth rate (CAGR) of 6.9% during the forecast period. This steady growth is driven by tightening NOₓ emission regulations globally (particularly in China, Europe, and North America), the expansion of the thermal power sector (especially in Asia), and increasing adoption of SCR technology in industrial sectors (cement, steel, petrochemicals, marine, glass).

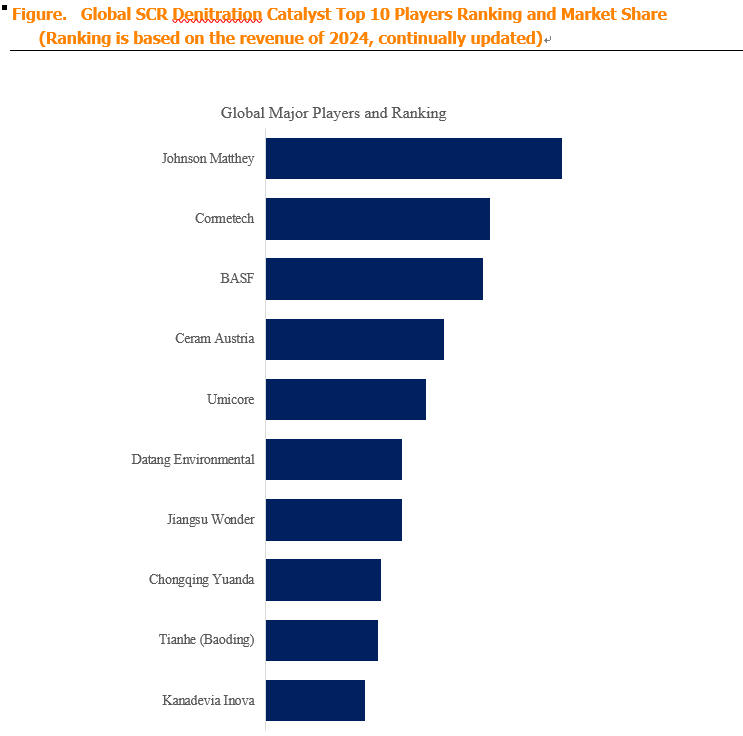

Market Monitor Global's analysis indicates that the global key manufacturers of SCR Denitration Catalysts include Johnson Matthey (UK), Cormetech (USA — a joint venture between Corning and Mitsubishi), BASF (Germany), Ceram Austria (Austria), Umicore (Belgium), Datang Environmental (China), Jiangsu Wonder (China), Chongqing Yuanda (China), Tianhe (Baoding) (China), and Kanadevia Inova (Switzerland/Japan). In 2024, the global top five players collectively accounted for approximately 37.0% of total revenue, indicating a moderately fragmented market with a mix of large multinational specialty chemical companies (Johnson Matthey, BASF, Cormetech) and numerous regional players (particularly in China, which has a large domestic market and many domestic manufacturers). The Chinese market is particularly fragmented, with many local suppliers competing on price, while multinational players dominate premium segments (high-efficiency catalysts, marine SCR, and high-value applications).

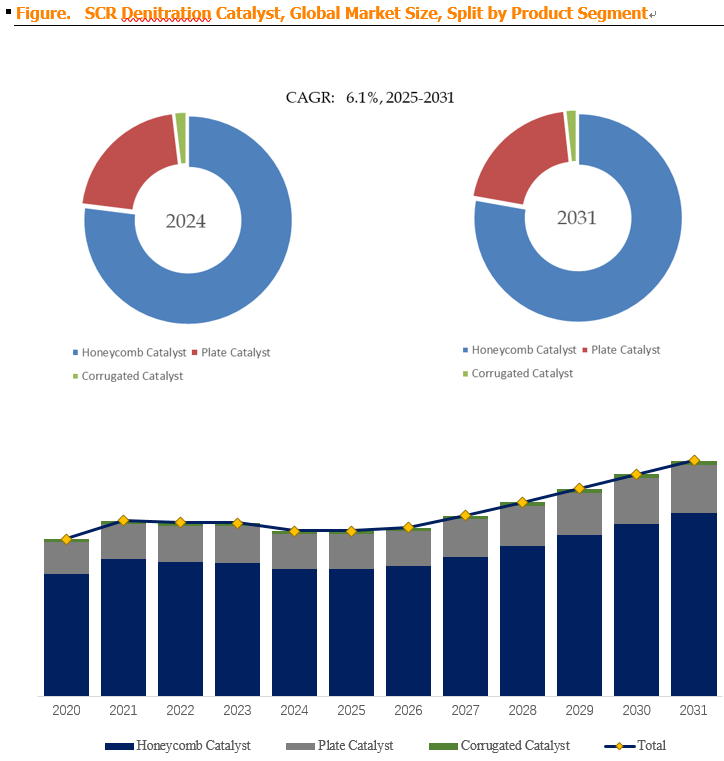

In terms of product type, Honeycomb Catalyst is currently the largest segment, holding a 77.0% share. Honeycomb extruded catalysts dominate the thermal power and industrial boiler markets due to their high surface area, low pressure drop, mechanical strength, and proven performance in high-dust applications. Plate Catalyst and Corrugated Catalyst account for the remaining share. Plate catalysts are used in some high-dust, high-erosion applications (e.g., certain coal-fired power plants), while corrugated catalysts are used in niche applications (e.g., some industrial processes, smaller units).

Regarding application, Thermal Power Plants is the largest segment, accounting for 51.0% of the market. Coal-fired, gas-fired, and oil-fired power plants are the primary users of SCR technology, as they are major NOₓ emitters and are subject to stringent emission limits (EU Industrial Emissions Directive, US EPA MATS, China's ultra-low emission requirements). Industrial Boilers (cement, steel, glass, petrochemicals, waste-to-energy) account for a significant share of the remainder. Marine (ships, large vessels) is a smaller but rapidly growing segment, driven by IMO Tier III NOₓ limits (mandated in Emission Control Areas, ECAs). Other applications (e.g., stationary engines, gas turbines, locomotives) represent the remainder.

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by China's massive installed capacity of coal-fired power plants (and the stringent "ultra-low emission" policy requiring NOₓ emissions < 50 mg/Nm³), rapid industrialization, and increasing environmental enforcement. China alone accounts for a substantial portion of global SCR catalyst demand. North America is a mature market, with steady demand from coal-fired power plants (though many are being retired, replaced by gas-fired plants, which still require SCR for NOₓ control), industrial boilers, and gas turbines. Europe is a mature market with strong regulatory drivers (Industrial Emissions Directive, national emission limits), high adoption of SCR in large power plants and industrial sectors. Rest of World (including Middle East, Africa, Latin America) represents smaller but growing markets, driven by infrastructure investment, industrial growth, and emerging environmental regulations.

SCR Denitration Catalyst Market Dynamics

Market Drivers:

-

D1: Tightening global NOₓ emission regulations – The primary driver for the SCR catalyst market is the ever-tightening regulatory landscape for NOₓ emissions. Key regulations include:

-

China: "Ultra-low emission" policy (2014 onwards) requires NOₓ emissions < 50 mg/Nm³ for coal-fired power plants, driving widespread SCR deployment and catalyst replacement cycles.

-

Europe: Industrial Emissions Directive (2010/75/EU) sets BAT (Best Available Techniques) standards for NOₓ emissions from large combustion plants. National regulations (e.g., Germany's TA Luft) impose strict limits.

-

US: Mercury and Air Toxics Standards (MATS) and Cross-State Air Pollution Rule (CSAPR) limit NOₓ emissions from power plants; EPA's regional haze rules require NOₓ controls on older plants.

-

IMO: MARPOL Annex VI Tier III limits NOₓ emissions in ECAs (North American ECA, North Sea ECA, Baltic ECA) to 2.0 g/kWh (applicable from 2016); new vessels in these areas require SCR or equivalent technology.

-

Other regions: Increasing NOₓ limits in India, South Korea, Japan, and other industrializing countries.

-

-

D2: China's coal-fired power capacity and "ultra-low emission" policy – China has the world's largest installed coal-fired power capacity (~1,100 GW) and consumes the majority of global coal. The "ultra-low emission" policy, which mandates NOₓ emissions < 50 mg/Nm³ (vs. ~200 mg/Nm³ previously), has driven massive SCR catalyst installations and replacement demand. Chinese domestic catalyst manufacturers have expanded rapidly to meet this demand, creating a large, competitive local market.

-

D3: Expansion of SCR to industrial sectors beyond power generation – While thermal power is the largest segment, SCR adoption is expanding in:

-

Cement production: New and revised cement industry emission standards (e.g., China's GB 4915-2013) require NOₓ control, driving SCR adoption.

-

Iron and steel: Sinter plants, blast furnaces, and coking plants are major NOₓ sources; regulations are tightening in China, India, and Europe.

-

Glass: Glass melting furnaces are high-temperature NOₓ sources; SCR is increasingly required in new installations and retrofits.

-

Petrochemicals: Refineries, chemical plants, and petrochemical complexes require NOₓ control on process heaters and boilers.

-

Marine: IMO Tier III NOₓ limits in ECAs are driving demand for SCR systems on new vessels and retrofits.

This diversification reduces dependence on the power sector and provides growth opportunities.

-

-

D4: Replacement demand from aging catalysts – SCR catalysts have a finite lifetime (3-8 years, depending on application). In power plants with SCR systems installed in the 2010s (driven by earlier regulations), the first generation of catalysts is reaching end-of-life and requires replacement. Replacement demand is now a significant portion of the market, providing a stable, recurring revenue stream for manufacturers.

-

D5: Growing demand for high-performance, low-temperature, and durable catalysts – To meet stricter emission limits, reduce operating costs, and extend catalyst life, there is increasing demand for:

-

High-efficiency catalysts (higher DeNOₓ conversion at lower NH₃ slip).

-

Low-temperature catalysts (operating at 170-250°C) enabling SCR placement downstream of dust removal equipment (lower dust, lower SO₂) but requiring catalysts with high activity at lower temperatures.

-

Poison-resistant catalysts: Catalysts less susceptible to poisoning by arsenic, phosphorus, alkaline metals, and other flue gas contaminants.

-

Low-SO₂ oxidation catalysts: Formulations that minimize SO₂ to SO₃ conversion, reducing corrosion and ammonium bisulfate fouling.

Manufacturers investing in R&D to develop such advanced catalysts can differentiate and command premium pricing.$1XY~NU6Y)G7ID.png)

-

Market Restraints:

-

R1: High manufacturing costs and material intensity – SCR catalysts are material-intensive:

-

TiO₂ (titanium dioxide): The primary support material, derived from titanium ore (ilmenite) or synthetic processes; TiO₂ prices are volatile and influenced by mining output, energy costs, and global supply-demand.

-

V₂O₅ (vanadium pentoxide): The active component, derived from vanadium sources; vanadium prices are volatile and driven by steelmaking demand (vanadium is a steel alloying element) and battery demand (vanadium flow batteries).

-

WO₃ (tungsten trioxide) or MoO₃ (molybdenum trioxide): Promoters to improve activity and thermal stability; prices are correlated with tungsten and molybdenum markets.

-

Energy: Catalyst production (mixing, extrusion, drying, calcination) is energy-intensive.

High material and energy costs constrain profit margins and make catalyst manufacturers vulnerable to raw material price volatility.

-

-

R2: Regulatory uncertainty and market concentration in China – While regulations drive demand, regulatory changes can impact the market. For example:

-

Slower-than-expected deployment of new coal-fired capacity due to climate policies (China, Europe, US).

-

Retirement of coal-fired power plants in developed countries (replaced by gas-fired, renewable energy), reducing the installed base requiring SCR.

-

Technology disruption: Alternative NOₓ control technologies (e.g., SNCR — selective non-catalytic reduction, low-NOₓ burners, or hybrid approaches) may compete with SCR in some applications.

Additionally, the Chinese market is dominated by numerous domestic manufacturers (many state-owned or subsidized), creating intense price competition and compressing margins for all players.

-

-

R3: Disposal and recycling challenges — Spent SCR catalysts contain vanadium (V₂O₅) and other heavy metals, classified as hazardous waste in many jurisdictions. Improper disposal can cause environmental contamination. While recycling is increasing (recovery of vanadium, tungsten, and titanium from spent catalysts), the logistics, processing costs, and regulatory compliance make disposal/recycling expensive. Some power plants delay catalyst replacement to reduce waste generation, impacting market demand.

Market Opportunities:

-

O1: Development of non-vanadium, non-toxic catalysts — Vanadium-based catalysts are effective but contain toxic V₂O₅, raising environmental and health concerns. R&D is progressing on non-vanadium SCR catalysts — for example:

-

Iron-based catalysts (Fe-zeolite): Active at higher temperatures, but may be less toxic and offer different performance characteristics.

-

Copper-based catalysts (Cu-zeolite): Active at low temperatures (150-300°C), promising for low-temperature SCR applications.

-

Manganese-based catalysts: Active at low temperatures, but may have lower SO₂ resistance.

-

Cerium-based catalysts: Oxidative catalysts, potentially with less toxicity.

While vanadium-based catalysts remain dominant due to their proven performance and cost-effectiveness, non-vanadium catalysts may gain share in applications where environmental toxicity is a concern (e.g., retrofit on densely populated areas, or in the future if regulations restrict vanadium use).

-

-

O2: Regeneration and recycling of spent catalysts — Spent SCR catalysts can be regenerated (cleaned and partially reactivated) rather than replaced entirely, extending useful life and reducing waste. Regeneration methods include:

-

Chemical washing: Removing accumulated poisons (arsenic, phosphorus, alkaline metals) and restoring activity.

-

Thermal treatment: Burning off carbon deposits or organic foulants.

-

Re-impregnation: Adding fresh active components (V₂O₅, WO₃) to restore activity.

Regeneration is cost-effective (30-60% of new catalyst cost), reduces waste, and aligns with circular economy principles. Manufacturers that invest in regeneration services can capture additional value and build customer loyalty.

-

-

O3: Expansion in marine SCR — IMO Tier III limits in ECAs (North America, North Sea, Baltic Sea) are driving demand for marine SCR systems. Marine SCR requires:

-

Compact, robust catalysts: Suitable for limited engine room space and operation on large vessels.

-

Low-temperature operation: Marine SCR operates at lower temperatures (e.g., 250-350°C) than power-plant SCR.

-

Compliance with marine regulations: Vessels must meet NOₓ emission limits during operation in ECAs; systems must be reliable and durable.

This is a higher-value, smaller-volume segment, with less price pressure than the power sector.

-

-

O4: Development of catalysts for biomass and waste-to-energy plants — Biomass and waste-to-energy plants often have more challenging flue gas composition (higher levels of alkali metals, chlorides, and other contaminants) than coal-fired plants. Catalysts for these applications must be more resistant to poisoning. As renewable energy and waste-to-energy capacity expands (driven by circular economy policies), demand for specialized SCR catalysts for these applications will grow.

-

O5: Catalyst solutions for small-scale and modular applications — Beyond large power plants, there is growing demand for SCR catalysts for small-scale and modular applications:

-

Distributed power generation: Small gas turbines, reciprocating engines, and combined heat and power (CHP) units.

-

Industrial boilers and process heaters: In manufacturing facilities.

-

Locomotives: Diesel locomotives in rail networks (where emission regulations are tightening).

-

Off-road equipment: Construction and mining equipment.

These applications require compact, modular catalyst designs, and often lower initial capital cost. Manufacturers that develop standardized, modular catalyst solutions can serve these growing segments.

-

}56LNJ.png)

Industry Trends:

-

Honeycomb catalyst dominance: Honeycomb extruded catalysts remain the dominant technology (77% share) due to their superior performance, low pressure drop, and proven track record.

-

Rising replacement demand: The installed base of catalysts (first-generation installed in the 2010s) is reaching end-of-life, creating stable replacement demand.

-

Expansion beyond thermal power: Increasing use of SCR in cement, steel, glass, petrochemicals, marine, and industrial boilers.

-

Low-temperature catalyst development: R&D on catalysts operating at 170-250°C to enable downstream SCR placement (lower dust, lower SO₂) and reduce energy costs.

-

Poison-resistant catalysts: Development of catalysts resistant to arsenic, phosphorus, alkaline metals, and other flue gas contaminants.

-

Regeneration and recycling: Growing focus on regenerating spent catalysts (reducing waste and cost) and recycling vanadium, tungsten, and titanium.

-

Consolidation in China: The highly fragmented Chinese market may see consolidation as larger players acquire smaller competitors, or as some smaller manufacturers exit due to price pressure and environmental regulations on their own production processes.