+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Material Handling Integration Market to Reach $6.65 Billion by 2031, Growing at 8.2% CAGR

Global Material Handling Integration Market to Reach $6.65 Billion by 2031, Growing at 8.2% CAGR

Monday,06 Jul,2026

Material Handling Integration: Definition and Principles

Material handling integration refers to the seamless incorporation of various components and systems involved in moving, storing, and controlling materials within a business operation. It entails the strategic coordination and synchronization of equipment, software, and processes to optimize these activities' efficiency, productivity, and safety.8CBJ(6Y9$}Z`XKM.webp)

Core objectives of material handling integration:

-

Streamline supply chains: Reduce bottlenecks, minimize delays, and enhance the flow of materials from receiving through storage, production, and shipping.

-

Reduce costs: Lower labor costs (through automation), reduce inventory carrying costs (through optimized storage), and minimize waste (damage, loss, misplacement).

-

Minimize errors: Improve accuracy in order fulfillment, inventory tracking, and material movement (reducing picking errors, mis-shipments, and inventory discrepancies).

-

Enhance operational performance: Increase throughput, improve on-time delivery, and enhance customer satisfaction.

-

Enable scalability and adaptability: Systems can be customized to meet the specific requirements of diverse industries, allowing businesses to handle diverse materials and accommodate changing production requirements. This flexibility enables businesses to adapt to market demands quickly and efficiently.

H3.png)

Key components of an integrated material handling system:

-

Hardware (largest segment, 63.3% share): Physical equipment used to realize material transmission, storage, sorting, loading, and unloading functions.

-

Conveyor systems: Belt, roller, chain, overhead, and modular conveyors.

-

Automated storage and retrieval systems (AS/RS): High-bay storage systems with automated cranes for storing and retrieving pallets, totes, and cartons.

-

Automated guided vehicles (AGVs) and autonomous mobile robots (AMRs): Mobile robots that transport materials along preset paths or autonomously navigate using sensors, cameras, and software.

-

Robotic arms: For picking, packing, palletizing, and sorting.

-

Sortation systems: Cross-belt sorters, tilt-tray sorters, and shoe sorters for distributing items to destinations.

-

Mezzanines, shelving, racking, and storage structures.

-

-

Software and control systems: The "brains" that orchestrate the hardware.

-

Warehouse management systems (WMS): Managing inventory, orders, and labor.

-

Warehouse control systems (WCS): Directly controlling and coordinating automated equipment.

-

Warehouse execution systems (WES): A hybrid layer managing real-time execution decisions (task prioritization, resource allocation).

-

Transportation management systems (TMS): Managing outbound shipping and freight.

-

Inventory management systems: Tracking stock levels, locations, and movements.

-

Analytics and reporting platforms: Providing insights into operational performance.

-

-

Integration layer: Interfaces, APIs, and middleware that connect hardware, software, and other enterprise systems (ERP, supply chain management, etc.).

Material Handling Integration Market Summary

According to a new market research report published by Market Monitor Global, the global Material Handling Integration market is projected to reach USD 6.65 billion by 2031, at a compound annual growth rate (CAGR) of 8.2% during the forecast period. This strong growth is driven by the rapid expansion of e-commerce, the increasing need for warehouse and distribution automation to manage labor shortages and rising labor costs, the adoption of Industry 4.0 technologies, and the growing demand for efficient, scalable, and flexible material handling solutions across various industries (retail, manufacturing, food & beverage, pharmaceuticals, automotive, logistics, etc.).

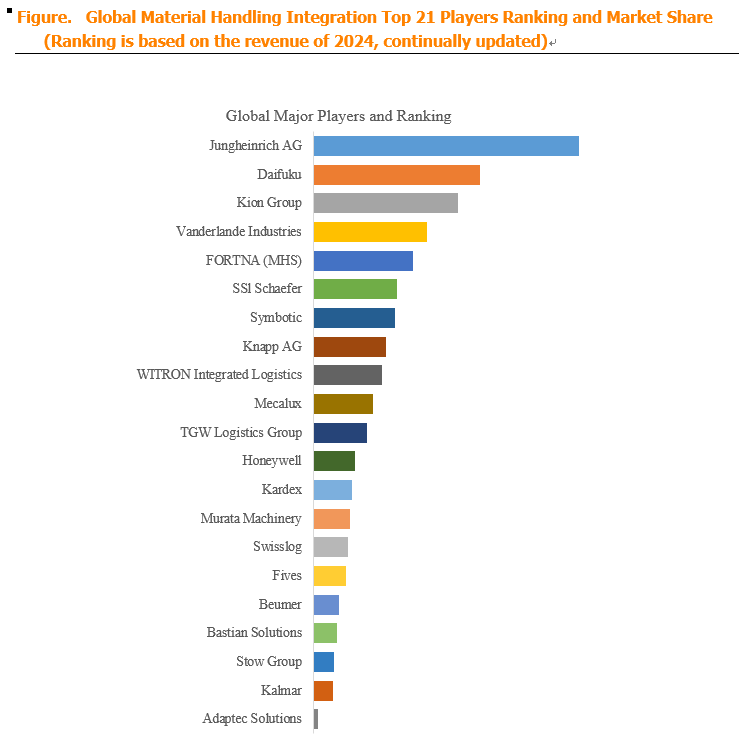

Market Monitor Global's analysis indicates that the global key manufacturers of Material Handling Integration include Jungheinrich AG (Germany), Daifuku (Japan), Kion Group (Germany), Vanderlande Industries (Netherlands), FORTNA (MHS) (USA), SSI Schaefer (Germany), Symbotic (USA), Knapp AG (Austria), WITRON Integrated Logistics (Germany), and Mecalux (Spain). In 2024, the global top 10 players collectively accounted for approximately 50.0% of total revenue, indicating a moderately concentrated market with several large, global system integrators and OEMs competing for large-scale projects. The market is characterized by significant M&A activity (consolidation to create "one-stop-shop" solutions), partnerships between integrators and OEMs, and the emergence of new technology providers (particularly in robotics and AI-driven software).

In terms of product type, Hardware is currently the largest segment, holding a 63.3% share. Hardware includes all physical equipment (conveyors, AS/RS, AGVs/AMRs, robotic arms, sorters, storage structures, etc.). While software and integration services are growing rapidly (as systems become more complex and digital), hardware still represents the majority of material handling integration project value (particularly for large-scale, greenfield projects). Software and Services (including WMS, WCS, integration services, consulting, and maintenance) accounts for the remaining share.

Regarding application, Retail & E-Commerce is the largest segment, accounting for 24.8% of the market. E-commerce fulfillment centers are among the most advanced and automated material handling environments, requiring high-speed sortation, dense storage, high-precision picking, and rapid order fulfillment. The growth of e-commerce (global e-commerce sales projected to exceed $8 trillion by 2027) is a primary driver for material handling integration investments. Food & Beverage, Manufacturing, Pharmaceuticals, Automotive, Logistics & Postal, and Others account for the remainder.

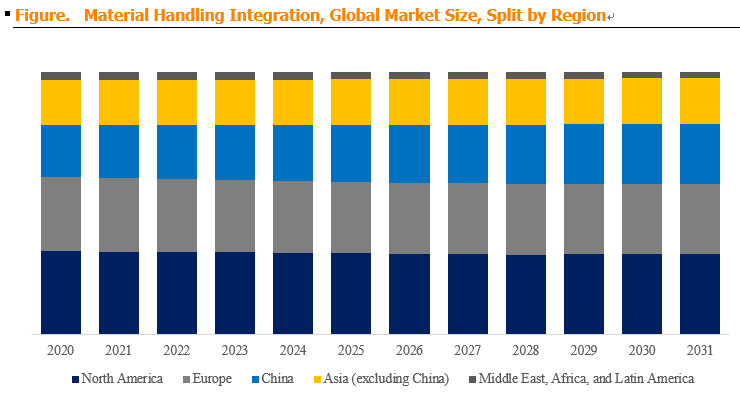

Regional dynamics: The shift toward increased automation is primarily occurring in the Americas and Europe, driven by the push to increase cost efficiencies in regions with higher input costs (labor costs, real estate costs). The North American market is the largest and fastest-growing, driven by strong e-commerce growth, labor shortages, and a large number of warehouse and distribution facility investments. Europe shows steady growth, driven by logistics automation in countries like Germany, the UK, and France, though market growth is slower than in North America due to lower impact of e-commerce (in some regions) and lower investments in infrastructure. Asia-Pacific is the fastest-growing region, driven by rapid industrialization, e-commerce growth (particularly in China, India, and Southeast Asia), increasing labor costs, and government initiatives for manufacturing and logistics modernization.

Y9$TF3VM.png)

Material Handling Integration Market Dynamics

Market Drivers:

-

D1: Growing trend toward integration of robotics and autonomous systems – Advanced robotic technologies, including autonomous mobile robots (AMRs), robotic arms, and automated storage and retrieval systems (AS/RS), are being incorporated into material handling systems to enhance efficiency, speed, and flexibility in warehouse and distribution operations. AMRs can navigate autonomously, avoiding obstacles and adapting to changing layouts; robotic arms can perform tasks such as picking, packing, palletizing, and sorting. These systems automate repetitive, physically demanding tasks, increasing productivity and reducing labor costs.

-

D2: Increasing global adoption of e-commerce – The explosive growth of e-commerce (online retail) is a significant catalyst for adopting material handling integration systems. With millions of shipped products globally daily, the demand for efficient material handling systems has skyrocketed. E-commerce fulfillment centers require high-speed, accurate order fulfillment — demanding advanced sortation, storage, and picking systems. In the fiercely competitive e-commerce industry, major players (Amazon, Alibaba, Walmart, etc.) rely heavily on these systems to enhance operational efficiency, reduce order cycle times, and maintain competitive advantage.

-

D3: Continuous progress of IoT, AI, and robotics – The advancement of enabling technologies provides the technical foundation for material handling integration:

-

IoT-enabled solutions: Real-time monitoring of material handling processes (equipment status, inventory levels, throughput). Sensors on conveyors, AGVs, and storage systems provide visibility into performance and enable predictive maintenance.

-

AI/ML for decision-making: Predictive maintenance (detecting equipment failures before they occur), real-time decision-making (task prioritization, resource allocation, dynamic routing), and dynamic inventory management (adjusting stock levels based on demand forecasts).

-

Robotics: Automating tasks such as picking, packing, and palletizing, improving intelligence and efficiency of material handling systems.

-

-

D4: Labor shortages and rising labor costs – The logistics and warehousing sector faces significant labor shortages, particularly in developed economies (US, Europe, Japan). Low unemployment rates, high turnover, and physical demands of warehouse work make recruiting and retaining staff challenging. Automation — through material handling integration — is essential for maintaining throughput, meeting customer expectations, and remaining competitive. Even in markets with lower labor costs (e.g., China, Southeast Asia), rising wages and increasing demand for productivity drive automation investment.

-

D5: Demand for flexibility, scalability, and resilience – Supply chain disruptions (COVID-19, geopolitical events, natural disasters, port congestion) have highlighted the need for resilient, flexible supply chains. Material handling integration enables:

-

Scalability: Systems can be expanded or reconfigured as business needs change (e.g., peak season capacity, new product lines).

-

Flexibility: Systems can handle diverse products (size, weight, shape, temperature sensitivity) and adapt to changing order profiles (e.g., shift from pallets to single-piece picking).

-

Resilience: Automated systems can operate 24/7 with fewer disruptions (labor strikes, illness, absenteeism).

3U54F0D}JCFW[FLF3.png)

-

Market Restraints:

-

R1: High capital expenditure and long ROI periods – Material handling integration projects (particularly large-scale, greenfield projects) require significant capital investment:

-

Hardware costs: Conveyors, AS/RS, AGVs, robots, sorters, storage structures.

-

Software costs: WMS, WCS, integration software, analytics platforms.

-

Integration costs: Engineering, installation, commissioning, testing.

-

Training and change management costs.

For small and medium enterprises, the upfront cost can be prohibitive. ROI periods may be 3-7 years, which may exceed management's investment horizon, or may not be justifiable in uncertain demand environments.

-

-

R2: Complexity of integration and implementation risks – Integrating multiple hardware and software components from different vendors (conveyors from one vendor, AS/RS from another, AGVs from a third, WMS from a fourth) is technically challenging:

-

System compatibility: Ensuring all components communicate seamlessly (interfaces, data exchange, protocols).

-

Performance validation: Ensuring the integrated system meets throughput, accuracy, and reliability specifications.

-

Risk management: Delays in equipment delivery, integration issues, software bugs, and unforeseen site conditions can cause project delays and cost overruns.

-

Skilled labor shortage: Designing, implementing, and managing integrated systems requires specialized engineering, project management, and IT expertise — which may be in short supply.

-

-

R3: Integration with legacy systems and brownfield sites – Many companies operate brownfield sites (existing warehouses/factories with legacy equipment and IT systems). Integrating new automation with legacy systems is often more difficult than greenfield (new build) projects. Challenges include:

-

Physical space constraints: Limited space for new equipment, requiring creative layouts or phased implementation.

-

Legacy equipment: Older equipment may not be compatible with modern controls and software.

-

Legacy IT systems: Older WMS or ERP systems may not support real-time communication with new automation.

-

Operational disruption: Implementing automation in an operational facility requires careful planning to minimize service disruption.

-

-

R4: Economic uncertainty and investment cycles – Material handling integration investments are correlated with economic cycles. In periods of economic downturn, companies may defer or cancel automation investments to preserve capital. Similarly, uncertainty around demand forecasts (e.g., post-COVID demand normalization) can delay investment decisions.

Market Opportunities:

-

O1: Creation of "one-stop solutions" – Winning companies will need to create "one-stop solutions" that rely on efficient models to facilitate easier delivery to customers. This includes:

-

Low-cost base: Efficient manufacturing, sourcing, and service delivery.

-

Capital expenditure dilution: Offering flexible financing models (leases, OPEX-based pricing).

-

Integrated offerings across adjacent subsegments: Offering multiple types of equipment and software from a single source (reducing integration risk for customers).

-

Strong joint ventures and partnerships with OEMs playing in adjacent segments.

-

Standardized and immediate-to-implement interfaces to enable equipment communication across multiple material-handling subsegments.

Ultimately, the goal is to provide seamless integration of all types and modes of material handling.

-

-

O2: Growth in emerging markets (Asia-Pacific, Latin America, Middle East) – Rapid industrialization, urbanization, and e-commerce growth in Asia-Pacific (particularly China, India, Indonesia, Vietnam, Thailand) and Latin America (Brazil, Mexico, Colombia) present significant opportunities. Companies with strong local presence, partnerships, and cost-effective solutions can capture market share.

-

O3: Adoption of micro-fulfillment and dark stores – As e-commerce delivery speed expectations increase (same-day, 2-hour, 1-hour delivery), retailers are deploying micro-fulfillment centers (small, automated warehouses located closer to customers) and dark stores (store-based fulfillment centers). These facilities require compact, highly automated, and cost-effective material handling integration solutions — creating opportunities for providers with modular, scalable solutions.

-

O4: Aftermarket services and retrofit upgrades – The installed base of material handling systems (conveyors, AS/RS, AGVs, sorters, WMS/WCS) is substantial and growing. Aftermarket services include:

-

Preventive and predictive maintenance: Regular inspection, service, and software updates.

-

Retrofit upgrades: Upgrading older systems with newer technologies (sensors, controls, software, robots) to extend useful life and improve performance.

-

Spare parts supply: Consumables, wear parts, and critical components.

-

Training and consulting: Operator training, system optimization, and continuous improvement programs.

Aftermarket revenue is typically higher-margin than equipment sales and provides recurring, predictable revenue.

-

-

O5: Digitalization and data-driven optimization – Beyond the physical integration of hardware, there is opportunity in digital solutions:

-

Digital twin: Simulating and optimizing material handling systems before they are built, and monitoring performance in real-time to identify optimization opportunities.

-

AI-driven analytics: Predictive maintenance, demand forecasting, inventory optimization, and real-time decision support.

-

Cloud-based WMS/WCS: Offering flexible, scalable, and lower-cost software solutions through the cloud.

These digital solutions enhance the value proposition of integration, improve customer outcomes, and provide recurring revenue streams.

-

Industry Trends:

-

Robotics integration (AMRs, robotic arms, collaborative robots): Increasing use of robotics for picking, packing, palletizing, and autonomous transport.

-

Artificial Intelligence (AI) and machine learning: For predictive maintenance, real-time decision-making, demand forecasting, and dynamic inventory management.

-

Internet of Things (IoT): Real-time monitoring of equipment and inventory, enabling predictive maintenance and proactive operations.

-

Micro-fulfillment and dark stores: Compact, automated facilities closer to customers for rapid delivery.

-

Automated storage and retrieval systems (AS/RS): High-density, high-speed storage for pallets, totes, and cartons — increasingly in flexible configurations (e.g., shuttle-based AS/RS).

-

Modular and scalable systems: Flexible systems that can grow with business needs, rather than requiring large upfront investments in fixed infrastructure.

-

Aftermarket and service contracts: Ongoing revenue from maintenance, upgrades, and optimization services.

-

One-stop solutions: System integrators offering comprehensive solutions (hardware + software + integration + aftermarket) from a single source, reducing risk and complexity for customers.