+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Global Synthetic Quartz Ingot Market to Reach $0.69 Billion by 2030, Growing at 4.9% CAGR

Monday,06 Jul,2026

Synthetic Quartz Ingot: Definition and Principles

Synthetic quartz ingots are high-purity, high-density materials extracted from quartz raw materials through precision technologies. The preparation process involves complex chemical and physical reactions to remove impurities from the raw materials, improve their purity, and achieve the required density and structure through specific processing means. The resulting material exhibits exceptional properties — including high thermal stability, excellent optical transparency (in the UV to IR range), low thermal expansion, high chemical purity, and outstanding electrical insulation — making it indispensable in semiconductor manufacturing, optical components, photovoltaic applications, and high-end laboratory equipment.

Key properties of synthetic quartz ingots:

-

High purity: Total impurity content (especially metal contaminants such as Na, K, Li, Fe, Cu, Al, Ca, Mg, Ti, etc.) is typically < 1 ppm for semiconductor-grade material. Ultra-high-purity grades (total impurities < 0.1 ppm) are used in extreme applications (EUV lithography, advanced semiconductor nodes).

-

Low thermal expansion coefficient: About 0.54 × 10⁻⁶ /°C (averaged over 0-100°C), providing excellent thermal shock resistance — critical for rapid thermal processing in semiconductor manufacturing and for high-power optical components.

-

High optical transparency: Transparent quartz (the dominant product type, 96.3% share) transmits UV, visible, and near-infrared light with minimal absorption or scattering. This is essential for photolithography, UV curing, and optical components.

-

Excellent chemical inertness: Resists most acids, alkalis, and solvents (except HF and hot phosphoric acid), making it suitable for corrosive environments (wet etching, chemical vapor deposition, and semiconductor processing).

-

High thermal stability: Use temperature up to 1,100–1,300°C (depending on grade), enabling use in high-temperature manufacturing processes.

-

Good dielectric properties: Low dielectric constant, low loss tangent, and high breakdown voltage — useful in high-frequency and high-voltage applications.

J$ECUZNY.png)

Production processes:

-

Natural quartz mining and purification: High-purity natural quartz is mined, crushed, and chemically purified (acid leaching, hot chlorination, etc.) to remove contaminants.

-

Melting: Purified quartz is melted in a high-temperature furnace (using plasma, electric arc, or flame fusion) to form a homogeneous, impurity-free glassy (amorphous) material.

-

Ingot formation: The molten quartz is cast or drawn into ingots (cylindrical or rectangular blocks) of precise dimensions, then annealed (slowly cooled) to relieve thermal stresses.

-

Synthesis (synthetic route): For ultra-high-purity applications, synthetic quartz is produced from silicon tetrachloride (SiCl₄) or siloxanes via chemical vapor deposition (CVD) or flame hydrolysis, yielding material with purity levels not achievable by melting natural quartz alone.

Product types:

-

Transparent Quartz (dominant, 96.3% share): Highly transparent, virtually bubble-free, and impurity-free. Used for optical windows, lenses, photolithography masks, and semiconductor crucibles.

-

Opaque Quartz: Contains minute bubbles or internal scattering centers; used for thermal insulation, furnace components, and applications where transparency is not required (e.g., furnace tubes, shielding).

-

Fused Silica / Fused Quartz: A broad category of amorphous quartz, including both transparent and opaque variants, produced by melting high-purity natural quartz.

YHF.png)

Synthetic Quartz Ingot Market Summary

According to a new market research report published by Market Monitor Global, the global Synthetic Quartz Ingot market is projected to reach USD 0.69 billion (approximately $690 million) by 2030, at a compound annual growth rate (CAGR) of 4.9% during the forecast period. This steady growth is driven by the expanding semiconductor industry (where quartz is essential for wafer processing), increasing demand for high-purity quartz in photovoltaics (solar cell manufacturing), and the growing use of quartz optics in high-end applications (lithography, laser systems, medical devices, and analytical instruments).

Market Monitor Global's analysis indicates that the global key manufacturers of Synthetic Quartz Ingots include Shin-Etsu Chemical (Japan), Feilihua (China), Heraeus Conamic (Germany/USA), Tosoh (Japan), and CoorsTek (USA). In 2024, the global top four players collectively accounted for approximately 79.0% of total revenue, indicating a highly concentrated market dominated by a few large, vertically integrated players with deep expertise in quartz synthesis, purification, and precision processing. Shin-Etsu is the market leader, offering a comprehensive range of synthetic quartz products for semiconductor, optical, and industrial applications. Feilihua (China) has emerged as a significant player, benefiting from China's semiconductor self-sufficiency push and strong government support for domestic supply chains.

In terms of product type, Transparent Quartz is currently the largest segment, holding a 96.3% share. The vast majority of synthetic quartz ingot demand is for transparent material, driven by its critical role in semiconductor wafer processing (crucibles, boats, tubes, and optical components) and high-end optics. Opaque Quartz accounts for the remaining share, used in niche applications requiring thermal insulation or resistance to aggressive environments.

Regarding application, Semiconductor is the largest segment, accounting for 80.7% of the market. Semiconductor applications include:

-

Quartz crucibles: High-purity quartz crucibles used in the Czochralski (CZ) process for growing single-crystal silicon ingots. Each crucible is used only once (or a few times) and is consumed during the process.

-

Quartz boats, tubes, and carriers: Used in diffusion, oxidation, annealing, and CVD (chemical vapor deposition) processes at high temperatures (900-1,200°C) in an inert or oxidizing atmosphere.

-

Photolithography: Quartz masks and optical components (lenses, windows, prisms) for deep UV (DUV) and extreme UV (EUV) lithography.

-

Wet processing: Quartz components for wet etching and cleaning, where chemical resistance is required.

The Photovoltaics (Solar) segment (use of quartz in solar cell manufacturing) and the Optics / Photonics segment (lenses, windows, prisms, waveplates, beam splitters) account for much of the remainder. Industrial, Medical, and Research/Academic applications represent smaller shares.

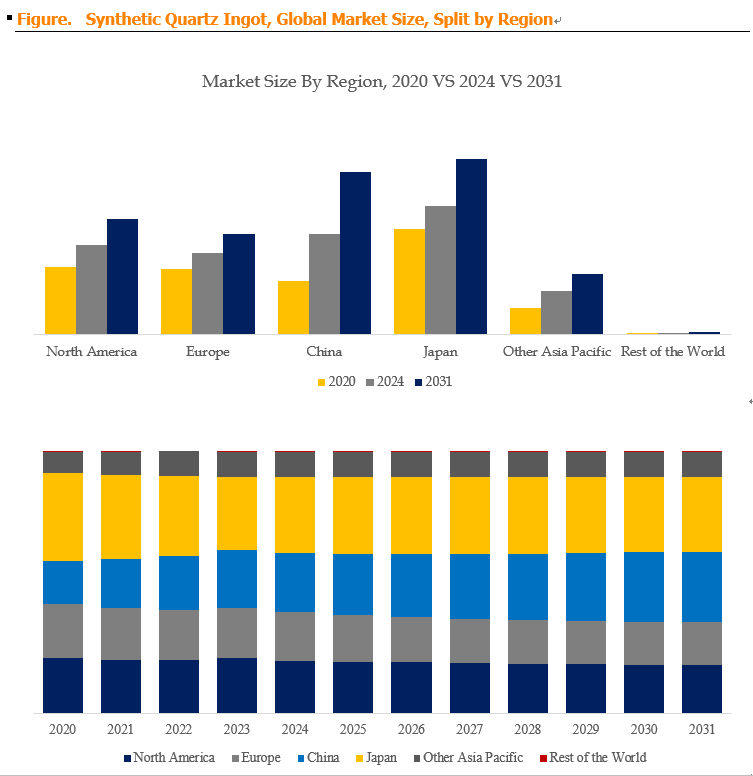

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by China's massive semiconductor industry expansion (with multiple new fabrication plants being built), Japan's leadership in semiconductor materials (Shin-Etsu, Tosoh), and Korea's strong semiconductor industry (Samsung, SK Hynix). North America is a mature market, driven by semiconductor manufacturing (Intel, TSMC in Arizona, GlobalFoundries, etc.), advanced optics (laser systems, aerospace), and research institutions. Europe is a stable market, with strong demand from the semiconductor industry, optics, and industrial applications. Rest of World (including the Middle East, Africa, and Latin America) represents smaller markets.

{ZD]ZQ1CAK.png)

Synthetic Quartz Ingot Market Dynamics

Market Drivers:

-

D1: Growing semiconductor industry and capacity expansion – The global semiconductor industry is experiencing robust growth, driven by the proliferation of AI, 5G, IoT, automotive electronics, and high-performance computing. Semiconductor fabrication facilities (fabs) require significant quantities of quartz components (crucibles, boats, tubes, carriers, optics). Each new fab built or existing fab expanded creates demand for synthetic quartz ingots, as these consumables are regularly replaced. Major announced investments in semiconductor manufacturing capacity — including TSMC (Taiwan, US, Japan), Intel (US, Europe), Samsung (Korea, US), SK Hynix (Korea), and numerous Chinese fabs — will drive demand for quartz over the forecast period.

-

D2: Demand for high-purity quartz in advanced semiconductor nodes – As semiconductor nodes shrink (from 5nm to 3nm, 2nm, and beyond), the purity requirements for quartz components become more stringent. Contamination from even trace amounts of metal impurities can cause device failures, yield loss, and reliability issues. Ultra-high-purity synthetic quartz (total impurities < 0.1 ppm) is required for EUV lithography, advanced deposition processes, and high-temperature oxidation/diffusion. This trend toward higher purity drives demand for premium-grade synthetic quartz ingots, which command higher prices.

-

D3: Growth of solar energy and photovoltaic manufacturing – The solar industry is expanding rapidly, driven by climate policies, declining costs, and energy security concerns. Solar cell manufacturing requires quartz components for:

-

Silicon wafer production: Quartz crucibles for the CZ process used in single-crystal silicon ingot production.

-

Diffusion and deposition processes: Quartz tubes, boats, and carriers for diffusion, oxidation, and PECVD (plasma-enhanced chemical vapor deposition).

-

Quartz plates and covers: Used in certain solar cell architectures.

While the solar segment is smaller than semiconductor, it is growing and provides an additional demand driver.

-

-

D4: Expanding optics and photonics markets – Advanced optical components — including laser systems, optical sensors, medical imaging devices, analytical instruments, and aerospace optics — rely on high-quality synthetic quartz. Key growth drivers include:

-

Medical lasers and surgical optics: For precision surgery, dermatology, and ophthalmology.

-

High-power laser systems: For industrial cutting, welding, and marking, and military applications.

-

Optical communication: Wavelength-selective switches, optical filters, and couplers.

-

Automotive and aerospace: LiDAR, sensors, and advanced driver assistance systems (ADAS).

The increasing adoption of these technologies drives demand for optical-grade synthetic quartz.

-

-

D5: Growing demand for quartz in EUV lithography – Extreme ultraviolet (EUV) lithography (used for advanced nodes 7nm and below) requires ultra-pure, ultra-low-defect quartz masks and optical components. EUV optics are made from ultra-low-expansion glass (ULE) or high-purity fused silica, with stringent requirements for thermal stability, homogeneity, and defect density. As EUV lithography scales to higher volume and more advanced nodes, demand for high-quality quartz masks and optical components will increase.

])IH6VKOEA`LQYD$UQJH.png)

Market Restraints:

-

R1: High production cost and capital intensity – Synthetic quartz ingot production is highly capital-intensive:

-

High-temperature furnaces: Melting and synthesis require expensive, high-temperature equipment (plasma torches, electric arc furnaces, CVD reactors).

-

Purification processes: Chemical purification, hot chlorination, and leaching require expensive chemicals, energy, and environmental controls.

-

Precision processing: Cutting, grinding, polishing, and annealing require advanced, high-precision equipment.

-

Quality control: Impurity analysis (ICP-MS, GD-MS), optical inspection, and defect testing add costs.

The high capital investment required limits the number of suppliers and creates high barriers to entry. New entrants face significant financial hurdles to establish production capacity and competitive quality.

-

-

R2: Limited availability of high-quality quartz raw materials – Natural quartz suitable for high-purity applications is limited and geographically concentrated (primarily in the US, Brazil, and China). Mining and purification of these high-quality ores are expensive and subject to environmental regulations. While synthetic quartz (CVD route) can reduce reliance on natural quartz, it is more expensive and requires different technical capabilities. This raw material dependency creates supply chain risk (geopolitical, regulatory, or environmental disruptions) and price volatility.

-

R3: Dependence on the semiconductor industry cycle – The semiconductor industry is cyclical, with periods of strong demand (expansion, capacity additions) followed by downturns (inventory corrections, demand softening). Synthetic quartz ingot demand is closely correlated with semiconductor capital expenditure and production volumes. During downturns, quartz demand declines, impacting revenue and profitability for quartz manufacturers.

-

R4: Competition from alternative materials – In some applications, synthetic quartz competes with alternative materials:

-

Alumina (Al₂O₃) ceramics: For high-temperature furnace components (where thermal shock resistance and chemical inertness are required, alumina is a cost-effective alternative for some applications).

-

Silicon carbide (SiC) ceramics: For high-temperature, high-corrosion applications (SiC components can operate at higher temperatures than quartz, but are more difficult to form and more expensive).

-

High-purity ceramics: For semiconductor processing, high-purity Al₂O₃, Y₂O₃, and other ceramics may substitute for quartz in certain applications (e.g., plasma-resistant components).

-

Glass alternatives: In optical applications, other high-transparency glasses (borosilicate, low-expansion glass) may substitute for quartz where extreme purity or UV transmission is not required.

However, for critical applications where ultra-high purity, UV transparency, and low thermal expansion are required, synthetic quartz remains irreplaceable.

-

Market Opportunities:

-

O1: Development of domestic quartz supply chains in China – China is investing heavily in semiconductor self-sufficiency, including domestic production of quartz components. Chinese quartz manufacturers (including Feilihua, and emerging players) are investing in capacity expansion and technology upgrades to reduce reliance on foreign suppliers (Shin-Etsu, Heraeus, Tosoh). This presents an opportunity for domestic suppliers to capture market share in the growing Chinese semiconductor and PV markets, and potentially export to other Asian markets.

-

O2: Increasing demand for ultra-high-purity (UHP) quartz for EUV and advanced nodes – As semiconductor technology pushes to 2nm, 1.4nm, and beyond, the purity requirements for quartz become more stringent. Ultra-high-purity synthetic quartz (total impurities < 0.1 ppm) will be required for EUV masks, advanced lithography optics, and critical process components. Manufacturers that can produce and qualify UHP quartz for advanced nodes can command premium pricing and build strong, defensible customer relationships.

-

O3: Customization and value-added processing – Beyond selling standard ingot shapes (cylindrical or rectangular), manufacturers can offer value-added processing:

-

Precision cutting and shaping: Ingots cut to customer-specified dimensions (crucible shape, boat geometry, tube dimensions, optical element blanks).

-

Annealing: Stress-relief annealing to reduce internal stress and improve performance.

-

Surface polishing: Providing high-quality surfaces for optical or semiconductor applications.

-

Custom shapes: Complex geometries for specialized applications (e.g., optical windows with custom curvature, diffusion tubes with integrated features).

These value-added services increase revenue per customer, improve customer loyalty, and differentiate from competitors.

-

-

O4: Expansion into specialty applications (biotechnology, analytical instruments) – Beyond semiconductor, solar, and optics, synthetic quartz is used in:

-

Biotechnology: Cuvettes, microfluidics, and labware for high-purity, UV-visible spectroscopy, and fluorescence applications.

-

Analytical instruments: Flow cells, reaction vessels, and detection windows for UV-Vis, HPLC, and other analytical techniques.

-

Medical devices: Components for surgical laser systems, diagnostic equipment, and therapeutic devices.

-

Semiconductor R&D and metrology: Specialized components for research institutions and pilot lines.

These specialty applications offer growth opportunities for manufacturers with flexible production and custom fabrication capabilities.

-

Industry Trends:

-

Ultra-high-purity (UHP) quartz development: Demand for UHP quartz is increasing for EUV lithography, advanced semiconductor nodes, and high-end optics.

-

Capacity expansion: Major players and new entrants are expanding production capacity to meet growing demand from semiconductor and solar industries.

-

Vertically integrated supply chains: Quartz manufacturers are investing in upstream raw material sourcing (natural quartz mines) and downstream processing (cutting, polishing, annealing, coating).

-

High-quality domestic production in China: Chinese quartz manufacturers are upgrading technology and capacity to serve domestic semiconductor and PV markets, reducing reliance on foreign suppliers.

-

Sustainability and green quartz production: Reducing energy consumption, water usage, and environmental footprint in quartz production is becoming increasingly important (responding to regulatory and customer ESG requirements).

Industry Structure and Competitive Dynamics

The global Synthetic Quartz Ingot market is characterized by:

-

Market leader (Shin-Etsu Chemical): Dominates with a comprehensive product portfolio, strong R&D, global manufacturing footprint, and long-standing relationships with leading semiconductor manufacturers. Known for ultra-high-purity materials and reliability.

-

Major Japanese players (Tosoh): Strong in high-purity quartz for semiconductor applications, optics, and industrial uses.

-

European and American players (Heraeus Conamic, CoorsTek): Strong in specialty applications (EUV optics, high-temperature components), with deep expertise in purification and processing.

-

Emerging Chinese players (Feilihua): Growing rapidly, benefiting from domestic semiconductor capacity expansion and government support. Feilihua is the leading domestic supplier and is expanding internationally.

-

Niche players: Companies specializing in specific applications (e.g., EUV optics, medical devices, analytical instrumentation).

Key success factors in this market:

-

Purity and quality: Ability to produce ultra-high-purity quartz with low impurity levels and consistent quality.

-

Technical expertise: Understanding of customer requirements (semiconductor fabrication, optical applications, PV manufacturing), and ability to customize products.

-

Manufacturing efficiency: Cost-effective production processes, high yield, and low defect rates.

-

Supply chain resilience: Access to high-quality raw materials, stable production capacity, and robust logistics.

-

Customer relationships: Long-term partnerships with semiconductor manufacturers and other key customers.