+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Library Automation Management System Market to Reach $1 Billion by 2030, Growing at 2.7% CAGR

Global Library Automation Management System Market to Reach $1 Billion by 2030, Growing at 2.7% CAGR

Friday,03 Jul,2026

Library Automation Management System: Definition and Principles

A Library Automation Management System (often referred to as an Integrated Library System, ILS, or Library Management System, LMS) is a type of automation software designed to manage core library operations. Its functionalities typically include acquisition (ordering and receiving library materials), cataloging (creating and maintaining bibliographic records), public access (online public access catalog, OPAC, enabling patrons to search and browse the collection), indexing and abstracting, circulation (check-in/check-out, reserves, fines management), serials management (tracking periodical subscriptions and issues), and reference services (managing reference inquiries and digital resources). Modern systems increasingly incorporate digital asset management (handling e-books, audiobooks, databases), discovery layers (unified search across multiple resources), and analytics (usage statistics, collection development analysis).PCW60A106{D0~EZWA_`_W.webp)

Core functional modules of a typical Library Automation Management System:

-

Acquisitions: Manages ordering, receiving, invoicing, and budgeting for library materials (books, journals, databases, multimedia). Integrates with vendor systems (EDI, EDI-X12) for automated ordering and invoice reconciliation.

-

Cataloging: Creates and maintains MARC (Machine-Readable Cataloging) records (MARC 21 format), metadata, authority control, and classification (Dewey Decimal, Library of Congress, etc.). Supports RDA (Resource Description and Access) standards and integration with national bibliographic utilities (OCLC, Library of Congress).

-

Circulation: Manages patron records, loans, renewals, holds, recalls, fines, and fees. Supports self-checkout kiosks, RFID inventory management, and patron communication (email/sms notifications). Integrated with library cards (barcode, RFID, mobile) for patron authentication.

-

Online Public Access Catalog (OPAC): Public-facing search interface enabling patrons to search the library catalog, view availability and location, place holds, renew items, and manage personal accounts. Modern OPACs include faceted search, relevance ranking, user reviews, and integration with discovery services.

-

Serials Management: Tracks serial publications (journals, magazines, newspapers) — issues, subscriptions, renewals, claims for missing issues, and binding. Integrates with EBSCO, ProQuest, and other serials vendors.

-

Reference and Digital Services: Manages reference inquiries, interlibrary loans (ILL), document delivery, and integration with digital repositories (institutional repositories, digital collections).

-

Administration and Reporting: System configuration (patron types, circulation policies, loan rules), security and access controls, and comprehensive reporting (circulation statistics, collection usage, patron demographics, budget tracking).

Key technology trends:

-

Cloud-based deployment: Hosted solutions (Software as a Service, SaaS) reduce on-premise IT costs, enable automatic updates, and provide anytime/anywhere access.

-

Open-source systems: Growing adoption of open-source ILS solutions (Koha, Evergreen) offering lower total cost of ownership and customization flexibility.

-

Mobile and patron-centric interfaces: Mobile apps, self-service portals, and digital-first experiences (e-books, e-audiobooks, streaming media).

-

AI and machine learning: Recommendation engines, automated metadata enrichment, chatbots for reference services, and predictive analytics for collection development.

-

Federated search and discovery: Unified search across multiple sources (library catalog, databases, open access repositories, internet resources).

GX07NE)NI0JRWQUJVY.png)

Library Automation Management System Market Summary

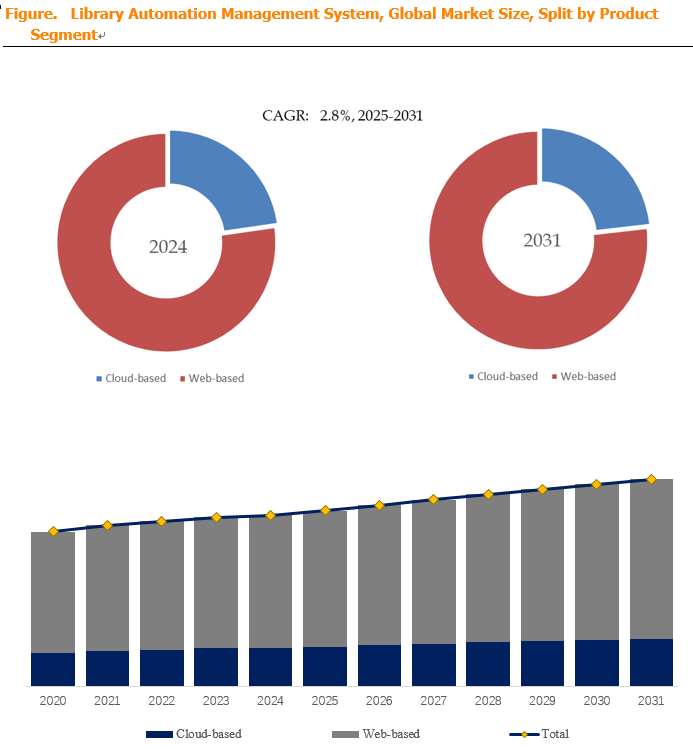

According to a new market research report published by Market Monitor Global, the global Library Automation Management System market is projected to reach USD 1 billion by 2030, at a compound annual growth rate (CAGR) of 2.7% during the forecast period. This steady growth is driven by the ongoing digitization of library services, the need for cost-effective and user-friendly library management solutions, and the increasing adoption of cloud-based and open-source platforms, particularly in educational and public library segments.

Market Monitor Global's analysis indicates that the global key manufacturers of Library Automation Management System include Clarivate (Ex Libris, Innovative Interfaces — including Sierra, Polaris, Vega), OCLC (WorldShare Management Services, WorldCat Discovery), SirsiDynix (Symphony, Horizon, Enterprise, BLUEcloud), Follett (Destiny, Destiny Discover), Axiell (Axiell Arena, Quria, V-smart), ParentPay (Library Management Cloud), Libsys (LibSys 10, LSEase), The Library Corporation (TLC's Library.Solution, CarlX), COMPanion (Alexandria), and Book Systems (Atriuum). In 2024, the global top five players collectively accounted for approximately 71.0% of total revenue, indicating a moderately concentrated market dominated by a few large, established vendors with extensive product portfolios and long-standing customer bases. However, the market is also witnessing increasing competition from smaller, niche, and open-source providers, particularly in certain regions and segments.

In terms of product type (by deployment model), the Cloud-based segment is the largest, holding a 22.7% share. Cloud-based systems are gaining significant traction due to their lower upfront capital costs, reduced IT maintenance burden, automatic updates, scalability, and remote accessibility. However, if we consider "Cloud-based" alongside "SaaS" and "Hosted" models, the actual market share is significantly higher and growing. The remaining segments include On-Premise and Open-Source (implemented on-premise or cloud-hosted).

Regarding application, School Libraries is the largest segment, accounting for 44.7% of the market. This includes K-12 school libraries (elementary, middle, high schools) and vocational/technical schools. School libraries are increasingly adopting library automation systems to manage growing collections, integrate with school management systems, and provide 24/7 access to digital resources for students and teachers. Academic Libraries (universities, colleges, research institutions) is the second-largest segment, driven by the need for complex cataloging, integration with academic systems, extensive e-resource management, and support for scholarly communication. Public Libraries (municipal, county, regional libraries) account for a significant share, with a focus on community engagement, digital inclusion, and ease of use for diverse patron populations. Special Libraries (corporate, law, medical, government, museum, archival) and Others account for the remainder.

Regional dynamics: North America is the largest market, driven by well-established public and academic library systems, high adoption of advanced library technologies (RFID, cloud, discovery layers), and significant IT spending. Europe is the second-largest market, with strong public library infrastructure and government support for digitization and open access initiatives. Asia-Pacific is the fastest-growing region, driven by increasing investments in education (particularly in China, India, Southeast Asia), government-led digitization programs, and rising internet penetration. Latin America and Middle East & Africa are smaller but growing markets, with increasing adoption of modern library management solutions as education systems expand.

F30J(Y80V4GTAGA(~EW.png)

Library Automation Management System Market Dynamics

Market Drivers:

-

D1: Digitization of library services and the shift to digital collections – Libraries are rapidly transitioning from physical collections (books, journals, multimedia) to digital content (e-books, e-journals, streaming media, audiobooks, databases). Automation systems must support the acquisition, management, discovery, and access of these digital resources. Additionally, the increasing demand for remote access (facilitated by the COVID-19 pandemic) has accelerated the adoption of cloud-based systems and mobile-accessible OPACs.

-

D2: Demand for cost efficiency and operational effectiveness – Libraries face pressure to reduce operational costs (staffing, physical infrastructure) while improving service quality. Automation systems streamline workflows (cataloging, circulation, acquisitions, serials), reduce manual labor, and improve efficiency. Automated notifications, self-service options, and integrated reporting reduce the burden on library staff, enabling them to focus on value-added services (reference, instruction, community outreach).

-

D3: Adoption of cloud-based and SaaS models – Cloud-based systems offer several advantages: lower upfront capital expenditure (no need for on-premise servers, IT infrastructure), predictable operating costs (subscription-based pricing), automatic updates (vendor-managed), high availability and disaster recovery, and easier scalability (adding libraries, branches, or users). This is particularly attractive for smaller libraries (school, special) and budget-constrained institutions. Major vendors are transitioning their product offerings to cloud/SaaS models (e.g., Ex Libris Alma, OCLC WMS, SirsiDynix BLUEcloud).

-

D4: Integration with institutional and educational systems – Library automation systems increasingly need to integrate with:

-

School management systems (e.g., student information systems, learning management systems) for student data synchronization, authentication, and single sign-on.

-

University information systems (e.g., student records, course management, faculty profiles) for seamless user experience.

-

Discovery services (EBSCO Discovery Service, Primo, Summon) for unified resource discovery.

-

Federated identity systems (Shibboleth, SAML, OAuth) for secure patron authentication.

Integration reduces administrative overhead, improves user experience, and increases the value of the automation system.

-

-

D5: Open-source alternatives driving innovation and competition – Open-source library automation systems (Koha, Evergreen, VuFind, etc.) provide cost-effective alternatives to commercial systems, particularly for budget-constrained libraries and consortia. Their availability drives commercial vendors to innovate, improve features, and offer competitive pricing. Open-source adoption is particularly strong in Europe and certain developing regions.

Market Restraints:

-

R1: High implementation and migration costs – Despite the availability of cost-effective cloud options, migrating from legacy systems to modern automation solutions can be costly and time-consuming:

-

Data migration: Transferring bibliographic records, patron data, circulation history, and configuration settings from old systems to new ones. Data cleaning, mapping, and verification require significant effort and expertise.

-

Staff training: Library staff must be trained on the new system, often requiring weeks or months of transition time.

-

Integration: Connecting the new system with existing institutional systems, discovery services, and third-party applications.

These costs can be prohibitive for small libraries with limited budgets, delaying adoption.

-

-

R2: Legacy systems and vendor lock-in – Many libraries have invested heavily in legacy automation systems over decades. Changing to a new system is disruptive and risky (potential data loss, operational disruption during transition). Additionally, vendor lock-in (difficulty in migrating data from proprietary systems) creates switching costs. This inertia slows the adoption of new technologies, particularly among larger academic and public libraries.

-

R3: Competition from open-source and free solutions – While open-source solutions drive innovation, they also create pricing pressure for commercial vendors. Budget-constrained libraries may opt for open-source solutions (even with higher implementation and support costs) over commercial subscriptions, reducing revenue for commercial vendors. This competition is particularly intense in the school library and special library segments.

-

R4: Rapid technological change and integration complexity – The library technology landscape is evolving rapidly: new standards (RDA, BIBFRAME), new discovery layers, AI/ML applications, privacy/security requirements, and integration with institutional ecosystems. Keeping up with these changes and ensuring seamless integration across multiple systems requires significant R&D investment from vendors. For smaller vendors, this can be challenging.

UHY74({XRHTRG4~L.png)

Market Opportunities:

-

O1: Artificial Intelligence and machine learning integration – AI/ML offers opportunities for library automation systems:

-

Recommendation engines: Personalized recommendations for patrons based on borrowing history, reading preferences, and peer usage.

-

Automated metadata generation: Using AI to enhance catalog records, suggest subject headings, and improve discoverability.

-

Chatbots and virtual reference: Automated answering of patron inquiries, reducing staff workload.

-

Predictive analytics: Forecasting demand, identifying collection gaps, optimizing acquisition budgets.

-

Digital preservation: Automated preservation workflows for digital collections.

Vendors that integrate robust AI/ML capabilities will differentiate themselves and command premium pricing.

-

-

O2: Mobile-first and patron-centric interfaces – Modern patrons expect mobile-responsive interfaces and convenient self-service options. Opportunities include:

-

Mobile apps: Check-out/check-in, renewals, holds, notifications, digital library access, event discovery.

-

Self-checkout and automated returns: Integration with self-checkout kiosks, RFID gates, and automated materials handling systems.

-

Patron-driven acquisition: Allowing patrons to suggest purchases, vote on acquisitions, or access on-demand digital content.

-

Personalized dashboards: Tailored user experiences based on patron type, preferences, and usage history.

Libraries that offer modern, user-friendly interfaces will attract and retain patrons.

-

-

O3: Cloud-native and microservices architectures – Vendors are transitioning from monolithic architectures to cloud-native, microservices-based platforms. Benefits include:

-

Scalability: Handle variable workloads (student arrivals, semester starts).

-

Resilience: Reduced downtime, rapid recovery from failures.

-

Faster feature development: Teams can develop and deploy new features independently.

-

Simplified integration: APIs for integration with other systems.

Cloud-native platforms will be better positioned for future innovation and interoperability.

-

-

O4: Open-source adoption and support services – Even as commercial vendors dominate, open-source adoption is growing. Opportunity exists for:

-

Open-source vendors/consultancies: Providing implementation, migration, customization, training, and support for open-source systems (Koha, Evergreen, etc.).

-

Hybrid models: Commercial vendors offering open-source products with paid support, hosting, and advanced features.

-

Consortia and shared services: Libraries collaborating to share open-source implementation and support resources, reducing individual costs.

This segment offers growth opportunities for specialized service providers.

-

-

O5: Expansion in emerging markets – Asia-Pacific, Latin America, and the Middle East are investing heavily in education and library infrastructure. Opportunities include:

-

Government-funded library digitization programs: National library networks, public library modernization, school library automation.

-

Greenfield projects: New libraries (academic, public) adopting modern automation systems from the start.

-

Low-cost cloud solutions: Targeting budget-constrained markets with affordable, feature-rich cloud-based systems.

-

Localization: Language support, local standards compliance, and regional customer support.

Vendors that adapt to emerging market needs can capture significant growth.

-

6CD2R}OOC(DQ~GZB8T.png)

Industry Structure and Competitive Dynamics

The global Library Automation Management System market is characterized by:

-

Dominant commercial vendors (Clarivate/Ex Libris/Innovative, OCLC, SirsiDynix, Follett): These companies have comprehensive product portfolios, large installed bases (thousands of libraries), global presence, and deep industry relationships. They dominate the academic library and large public library segments.

-

Regional leaders (Axiell in Europe, Libsys in India, The Library Corporation in North America): Strong regional presence, often with specialized products tailored to local needs and regulations.

-

Niche and specialty vendors: Companies focusing on specific library types (school, special, law, medical), specific functional areas (discovery, digital asset management, consortia management), or specific technologies (RFID, open-source).

-

Open-source providers (Koha, Evergreen) and their support ecosystems: Not for-profit vendors in the traditional sense, but they influence the market by offering alternatives and driving pricing competition.

Key success factors in this market:

-

Product maturity and functionality: Comprehensive coverage of library management functions, robust reporting, and analytics.

-

User experience: Intuitive, modern interfaces for both library staff and patrons.

-

Integration and interoperability: Seamless integration with institutional systems, discovery services, and third-party applications.

-

Cost-effectiveness: Competitive pricing, transparent cost models, and low total cost of ownership.

-

Customer support and training: Responsive support, comprehensive training, and extensive documentation.

-

Innovation and R&D: Continuous improvement, adoption of new technologies (AI, cloud, mobile), and staying ahead of industry trends.

-

Local presence and domain knowledge: Understanding local library practices, regulations, and language requirements.