+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Enteral Nutritional Products Market to Reach $5.09 Billion by 2031, Growing at 4.6% CAGR

Global Enteral Nutritional Products Market to Reach $5.09 Billion by 2031, Growing at 4.6% CAGR

Friday,03 Jul,2026

Enteral Nutritional Products: Definition and Principles

Enteral nutrition (EN) is a nutritional preparation with complete nutritional ingredients, designed to provide the necessary nutrients and energy for the human body and meet the patient's requirements for essential amino acids, essential fatty acids, vitamins, minerals, and trace elements. The nutrients contained in these products are derived from natural foods, with ingredients similar to those in a normal human diet, and have no toxic side effects on the human body. Enteral nutritional products are administered via the gastrointestinal tract (GI) through oral intake or tube feeding (nasogastric, nasoenteric, gastrostomy, or jejunostomy tubes) when a patient cannot consume adequate nutrition by mouth due to illness, injury, or surgery.

Key categories of enteral nutritional products:

-

Standard (Polymeric) Formulas: For patients with intact GI function. Contain whole proteins, complex carbohydrates, and fats. Examples: Ensure®, Nutren®, Fresubin®.

-

Elemental and Semi-Elemental Formulas: For patients with impaired digestion or absorption (e.g., short bowel syndrome, pancreatitis). Contain predigested nutrients (amino acids, peptides, simple sugars, medium-chain triglycerides MCTs) for easy absorption.

-

Disease-Specific Formulas: Tailored for specific conditions — renal disease (lower protein, electrolytes), hepatic disease (branched-chain amino acids), diabetes (low glycemic index), pulmonary disease (higher fat, lower carbohydrate to reduce CO₂ production), critical care (immune-modulating formulas with arginine, glutamine, omega-3 fatty acids).

-

Pediatric Formulas: For infants and children, matching growth and developmental needs.

-

Specialty Formulas: For metabolic disorders (e.g., phenylketonuria, PKU), food allergies, or intolerance (e.g., lactose-free, gluten-free).

Key product formats (by packaging):

-

Plastic Bottles (largest segment, 47.2% share): Ready-to-use liquid formulas in PET or polyethylene bottles, in sizes ranging from 200 ml to 1,000 ml. These are convenient for oral consumption and direct tube attachment.

-

Cans / Tins: Sterilized liquid or powdered formulas in metal cans.

-

Pouches / Bags: Sterile, flexible plastic bags for tube feeding (often used in hospital settings via enteral feeding pumps).

-

Powders (Sachets / Bulk): Reconstitutable powders for mixing with water — used in home care and institutional settings where storage space is limited or for cost reasons.

-

Ready-to-Drink (RTD) Cartons: Single-serve cartons (200 ml, 250 ml, 330 ml) for oral supplementation.

Key clinical applications:

-

Critical Care / Hospital Inpatients: For patients in ICU, post-surgery, trauma, burns, sepsis, and other acute conditions.

-

Chronic Disease Management: Cancer (cachexia prevention), neurological disorders (stroke, Parkinson's, ALS, multiple sclerosis), renal disease, liver disease, COPD.

-

Geriatric Nutrition: Aging populations with reduced appetite, swallowing difficulties (dysphagia), dental issues, or frailty.

-

Pediatric Nutrition: Premature infants, failure to thrive, cystic fibrosis, genetic disorders.

-

Home Enteral Nutrition: Long-term, home-based tube feeding or oral supplementation.

Enteral Nutritional Products Market Summary

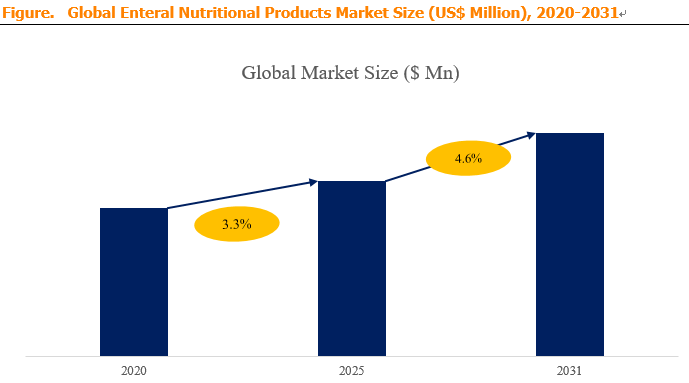

According to a new market research report published by Market Monitor Global, the global Enteral Nutritional Products market is projected to reach USD 5.09 billion by 2030, at a compound annual growth rate (CAGR) of 4.6% during the forecast period. This steady growth is driven by the rising prevalence of chronic diseases, aging populations, the expansion of home healthcare, increasing hospital admissions, and growing awareness of the clinical benefits of enteral nutrition.

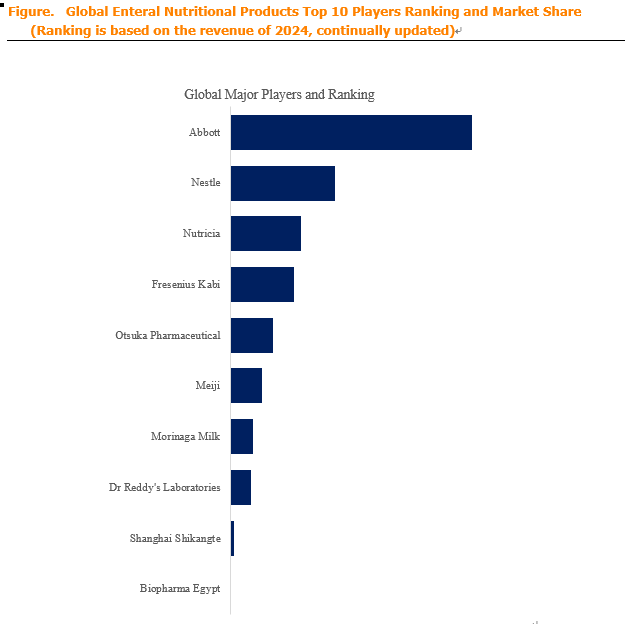

Market Monitor Global's analysis indicates that the global key manufacturers of Enteral Nutritional Products include Abbott (USA), Nestlé (Switzerland), Nutricia (Netherlands — a Danone company), Fresenius Kabi (Germany), Otsuka Pharmaceutical (Japan), Meiji (Japan), Morinaga Milk (Japan), Dr Reddy's Laboratories (India), Shanghai Shikangte (China), and Biopharma Egypt (Egypt). In 2024, the global top five players collectively accounted for approximately 64.0% of total revenue, indicating a moderately concentrated market with a few large multinational players dominating premium, clinically validated, and high-growth segments. The market is characterized by intense competition in the standard formula segment and strong differentiation in specialty formulas.

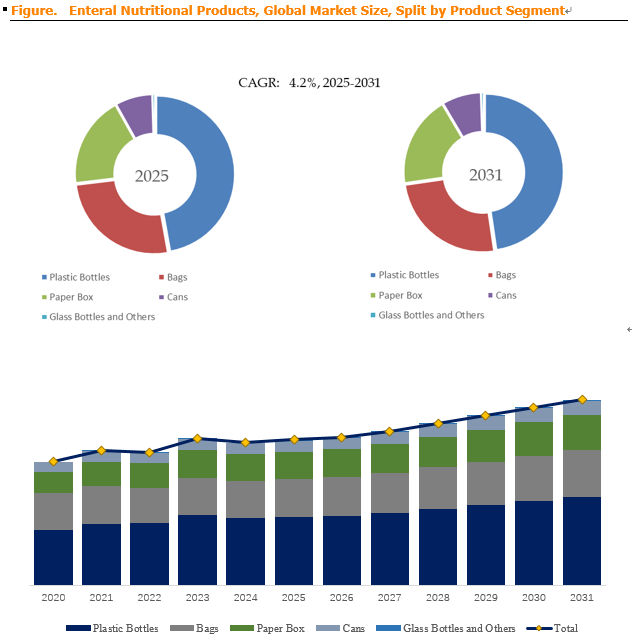

In terms of product type (by packaging), Plastic Bottles is the largest segment, holding a 47.2% share. Plastic bottles (PET, HDPE) are lightweight, shatter-proof, convenient for both oral and tube feeding, and widely accepted by patients and healthcare providers. Cans and Pouches/Bags are significant, particularly in hospital-based tube feeding. Powder and Ready-to-Drink Cartons account for the remainder, with powders dominating in cost-sensitive and home-care segments.

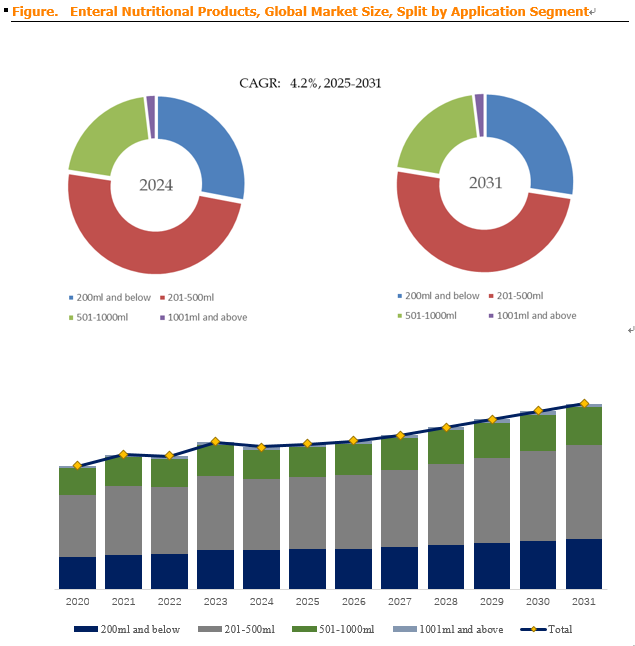

Regarding application (by volume or product size), 200ml and below is the largest segment, holding a 28.0% share. Small-volume products (200 ml, 250 ml, 330 ml) are convenient for oral supplementation, single-use tube feeding in hospitals, and for patients with reduced appetite or small gastric capacity. 500ml and 1000ml sizes are also significant for larger-volume tube feeding (especially in hospital and long-term care settings), with 1000ml+ used in high-volume continuous tube feeding (e.g., ICU, long-term care).

Regional dynamics: Asia-Pacific is the fastest-growing region, driven by aging populations in Japan, South Korea, and China; expanding healthcare infrastructure in China, India, and Southeast Asia; and rising awareness of clinical nutrition. North America and Europe are mature markets with steady growth, driven by chronic disease prevalence, home enteral nutrition, and reimbursement policies that support outpatient nutrition support. Latin America and Middle East & Africa are emerging markets with improving healthcare access and increasing adoption of enteral nutrition in hospitals.

Enteral Nutritional Products Market Dynamics

Market Drivers:

-

D1: Rising prevalence of chronic diseases and aging populations – The global burden of chronic diseases (cardiovascular disease, cancer, diabetes, COPD, neurological disorders) is increasing, driven by aging populations and lifestyle changes. These conditions often lead to malnutrition, weight loss, and reduced quality of life, requiring enteral nutritional support. The global population aged 65+ is projected to double from 750 million (2020) to 1.5 billion (2050), driving sustained demand.

-

D2: Increasing hospital admissions and critical care demand – Rising surgical volumes (orthopedic, cardiovascular, oncological, gastrointestinal) and ICU admissions (sepsis, trauma, burns, stroke) create demand for enteral nutrition for patients unable to eat orally. As healthcare systems expand capacity (particularly in emerging economies), enteral nutrition becomes a standard component of care.

-

D3: Expansion of home enteral nutrition (HEN) – With the shift from hospital to home-based care (reducing costs, improving patient quality of life), home enteral nutrition is growing rapidly. Patients with chronic conditions (cancer, neurological diseases, digestive disorders) can be discharged home with enteral feeding support (tube feeding, oral supplements). Advances in home infusion technology, education, and reimbursement policies are driving this trend.

-

D4: Growing awareness of the clinical benefits of enteral nutrition – Enteral nutrition is increasingly recognized for its benefits: maintaining gut integrity (preventing bacterial translocation), reducing hospital-acquired infections, improving wound healing, lowering mortality, and shortening hospital stay lengths. Clinical guidelines (ESPEN, ASPEN) recommend early enteral nutrition in critically ill patients.

-

D5: Technological advances in product formulations – New formulations are being developed: high-protein, high-energy, low-volume (for patients with limited capacity); immune-modulating formulas (with glutamine, arginine, omega-3); disease-specific formulas (renal, hepatic, pulmonary, diabetic); and organic, non-GMO, or plant-based formulas (growing consumer preference). These innovations enable better patient outcomes and broader patient eligibility.

Market Restraints:

-

R1: High cost and reimbursement limitations in many regions – Enteral nutritional products can be expensive, particularly specialty formulas and ready-to-use liquid products. Reimbursement policies vary widely: in many countries, enteral nutrition is partially or not reimbursed, limiting access for lower-income patients. In developed countries, reimbursement (health insurance, government programs) is generally available but often limited to specific diagnoses and settings. Cost pressure on healthcare budgets (especially in public systems) can restrict use or lead to formulary restrictions.

-

R2: Clinical complications and safety concerns – Enteral nutrition is not without risks: aspiration pneumonia (particularly with tube feeding in patients with reduced consciousness), gastrointestinal issues (diarrhea, constipation, bloating, gastroparesis), tube occlusion, metabolic complications (refeeding syndrome, electrolyte imbalances, hyperglycemia). These complications require careful patient selection, monitoring, and formulation choice. Lack of trained healthcare professionals (especially in home settings) can lead to adverse events, limiting market growth.

-

R3: Intense competition and pricing pressure – The enteral nutritional products market is highly competitive, with multiple major players and many smaller regional/national companies. In standard formula segments, products are relatively undifferentiated, leading to price competition and margin pressure. Hospitals and healthcare systems increasingly use tenders and group purchasing to drive down prices.

Market Opportunities:

-

O1: Growing demand for plant-based and specialized formulas – Consumers are increasingly interested in plant-based nutrition. Enteral nutrition products with plant-based protein sources (soy, pea, rice, hemp) and organic ingredients are an emerging segment. Clinical formulas addressing specific conditions (diabetes, renal disease, liver disease) are also growing, as they enable better clinical outcomes and can command premium pricing.

-

O2: Expansion of enteral nutrition in oncology – Cancer patients often suffer from malnutrition, cachexia (muscle wasting), and reduced food intake due to the disease itself (tumor metabolism) and/or treatment side effects (chemotherapy-induced nausea, mucositis, appetite loss). Enteral nutrition improves treatment tolerance, reduces treatment interruptions, and improves quality of life. Demand from oncology settings is growing as treatment regimens intensify and supportive care becomes more comprehensive.

-

O3: Home enteral nutrition (HEN) expansion – Home enteral nutrition is a high-growth segment, driven by patient preference, cost savings for healthcare systems, and technological advances. Opportunities include:

-

Patient education and training programs.

-

Telemedicine and remote monitoring for HEN patients.

-

Home delivery of products and consumables (feeding pumps, tubes, syringes, cleaning supplies).

-

Integration with digital health platforms for symptom tracking and nutrition monitoring.

-

-

O4: Emerging markets (Asia-Pacific, Latin America, Middle East) – As healthcare systems in these regions expand, enteral nutrition is becoming a standard part of care in hospitals and, increasingly, in home settings. Local manufacturing and product development (culturally appropriate products, targeted pricing) are opportunities for both multinational and local companies.

-

O5: Digital health integration — smart feeding pumps and monitoring systems – Enteral nutrition feeding pumps with connectivity (Wi-Fi, Bluetooth) enable remote monitoring, dose tracking, and real-time symptom management. Integrated digital health platforms can improve patient outcomes and reduce healthcare utilization, making enteral nutrition more effective and cost-efficient.

Industry Structure and Competitive Dynamics

The global Enteral Nutritional Products market is characterized by:

-

Global leaders (Abbott, Nestlé, Nutricia/Danone, Fresenius Kabi): These companies have extensive product portfolios, strong R&D, global supply chains, and long-standing relationships with healthcare providers and hospitals. They dominate premium, clinically validated, and disease-specific segments.

-

Regional players: Companies like Otsuka (Japan), Meiji (Japan), Morinaga (Japan), Dr Reddy's (India), Shanghai Shikangte (China), and Biopharma Egypt (Egypt) — serving their domestic and regional markets with cost-effective, culturally appropriate products. Some are expanding internationally.

-

Niche players: Smaller companies focusing on specialized formulations (organic, vegan, disease-specific) or specific delivery technologies (powders, liquid, tube feeding systems).

Key success factors in this market:

-

Clinical evidence: Strong clinical trial data demonstrating safety, efficacy, and outcomes for specific patient populations.

-

Product quality and formulation: High-quality ingredients, stability, palatability, and compatibility with enteral feeding systems.

-

Regulatory compliance: Adherence to FDA, EMA, and other regulatory standards; ability to navigate complex registration processes (particularly for novel formulations).

-

Distribution network: Effective hospital, pharmacy, and home care channels; strong relationships with healthcare providers.

-

Reimbursement support: Experience navigating reimbursement systems and providing support to patients and healthcare providers for reimbursement claims.

-

Innovation: Continuous R&D for new products, delivery systems, and application areas.