+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Ethylene Acrylic Acid Copolymers Market to Reach $0.43 Billion by 2030, Growing at 9.9% CAGR

Global Ethylene Acrylic Acid Copolymers Market to Reach $0.43 Billion by 2030, Growing at 9.9% CAGR

Friday,03 Jul,2026

Ethylene Acrylic Acid Copolymers: Definition and Principles

Ethylene acrylic acid copolymers (EAA) are produced by the high-pressure copolymerization of ethylene with acrylic acid in the presence of a free-radical initiator. This polymerization process creates a versatile family of polymers with a unique combination of properties derived from the two monomers:

-

Ethylene contributes flexibility, low-temperature toughness, and hydrophobicity.

-

Acrylic acid provides polarity, adhesion, and reactivity (via the carboxyl group).

The ratio of acrylic acid in the copolymer typically ranges from 5% to 20% by weight (and up to 30% in some specialized grades), allowing manufacturers to tailor the material's properties for specific applications.

Key properties of EAA:

-

Excellent adhesion to polar substrates: The carboxyl groups (-COOH) in EAA create strong hydrogen bonding and ionic interactions with polar surfaces such as aluminum foil, metals, paper, glass, and nylon. This adhesion persists even in moist or humid conditions, making EAA an ideal tie-layer adhesive in multi-layer packaging structures.

-

Good sealing properties: EAA forms strong, durable heat seals across a wide temperature range. It has excellent hot-tack strength (adhesion immediately after sealing) and maintains seal integrity under stress.

-

Flexibility and toughness: EAA retains flexibility and impact resistance at low temperatures (down to -40°C) while maintaining toughness. This makes it suitable for applications requiring cold-temperature performance (e.g., frozen food packaging).

-

Chemical resistance: EAA offers good resistance to oils, greases, acids, bases, and many solvents — important for food packaging and industrial applications.

-

Special hardness: EAA's hardness can be tailored from semi-flexible to rigid, depending on the acrylic acid content. This range of hardness makes it suitable for applications from flexible films to rigid containers.

-

Compatibility with other polymers: EAA can be blended with other polymers (polyethylene, polypropylene, copolymers) to enhance adhesion, heat seal properties, or mechanical performance.

-

Transparency: EAA can be processed into clear films and coatings, suitable for packaging applications where product visibility is desired.

Key processing methods:

-

Extrusion (dominant, 86.2% of market): EAA is widely used in extrusion processes, including film extrusion (blown film, cast film), extrusion coating, and co-extrusion. In co-extrusion, EAA is often used as a tie layer between incompatible polymer layers (e.g., LDPE and EVOH, LDPE and aluminum, PET and PE).

-

Blow molding: For bottles, containers, and industrial parts.

-

Injection molding: For caps, closures, and industrial components.

-

Powder coating: EAA can be ground into powder for coating applications.

Key applications:

-

Packaging (largest segment, 67.7% share):

-

Food packaging: Laminates for meats, cheese, snacks, frozen foods, liquids (juice, milk), and retort pouches. EAA ensures strong seal integrity and prevents delamination.

-

Liquid packaging: Milk, juice, and beverage cartons (e.g., Tetra Pak) where EAA is used as an adhesive tie layer between paperboard, aluminum foil, and polyethylene.

-

Shrink films: For wrapping and bundling.

-

Industrial packaging: For heavy-duty sacks, liners, and protective packaging.

-

Peelable seal layers: Used in easy-open packaging (e.g., lidding films, blister packs).

-

-

Adhesives and sealants: EAA is used in hot melt adhesives, pressure-sensitive adhesives, and as a binder in construction materials.

-

Coatings: EAA-based coatings are used on metals (corrosion protection), on paper (grease resistance), and on textiles (water repellency).

-

Automotive: EAA is used in underbody coatings, interior trim, and as an adhesive in composite panels.

-

Extrusion coatings for paper and board: EAA-coated paper and board are used for fast-food packaging, cups, plates, and other disposable foodservice items.

-

Specialty applications: EAA-based ionomers (partially neutralized with metal ions, e.g., sodium or zinc) are used in golf ball covers, sport equipment, and automotive parts.

Ethylene Acrylic Acid Copolymers Market Summary

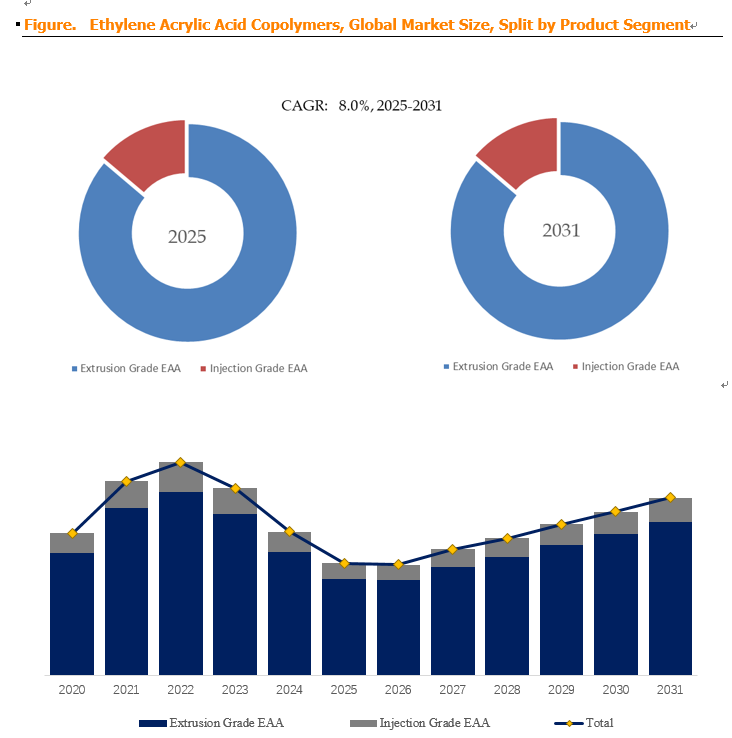

According to a new market research report published by Market Monitor Global, the global Ethylene Acrylic Acid Copolymers market is projected to reach USD 0.43 billion by 2030, at a compound annual growth rate (CAGR) of 9.9% during the forecast period. This strong growth reflects the increasing demand for high-performance packaging materials (particularly flexible packaging with barrier and adhesive properties), the shift toward lightweight and sustainable packaging structures, and the growing use of EAA in emerging applications.

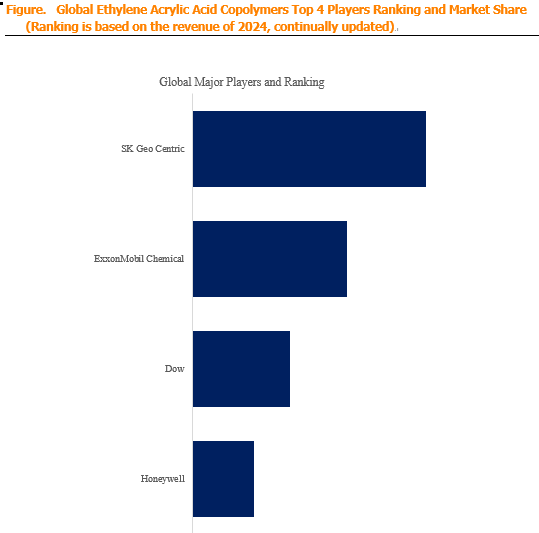

Market Monitor Global's analysis indicates that the global key manufacturers of Ethylene Acrylic Acid Copolymers include SK Geo Centric (South Korea) and ExxonMobil Chemical (USA). In 2024, the global top three players collectively accounted for approximately 85.0% of total revenue, indicating a highly concentrated market with a small number of large producers. The high concentration is due to the technical complexity of high-pressure EAA polymerization, the need for specialized production facilities (autoclave or tubular reactors), and the significant scale required to be cost-competitive. Other players (e.g., Dow, LyondellBasell, and smaller regional producers) account for the remaining share.

In terms of product type, Extrusion Grade EAA is currently the largest segment, holding an 86.2% share. Extrusion grade EAA is used in co-extrusion, extrusion coating, and blow molding applications — representing the dominant processing methods for EAA. Extrusion grades are optimized for film and coating applications, offering good melt flow, thermal stability, and adhesion. Adhesive Grade and Coating Grade (powder coating) account for the remaining share.

Regarding application, Packaging is the largest segment, accounting for 67.7% of the market. Within packaging, Flexible Packaging (films, pouches, laminates) is the dominant sub-segment, followed by Liquid Packaging (cartons), Shrink Films, and Industrial Packaging. The remaining applications include Adhesives and Sealants, Coatings (paper, metal, textile), Automotive, Construction, and Others.

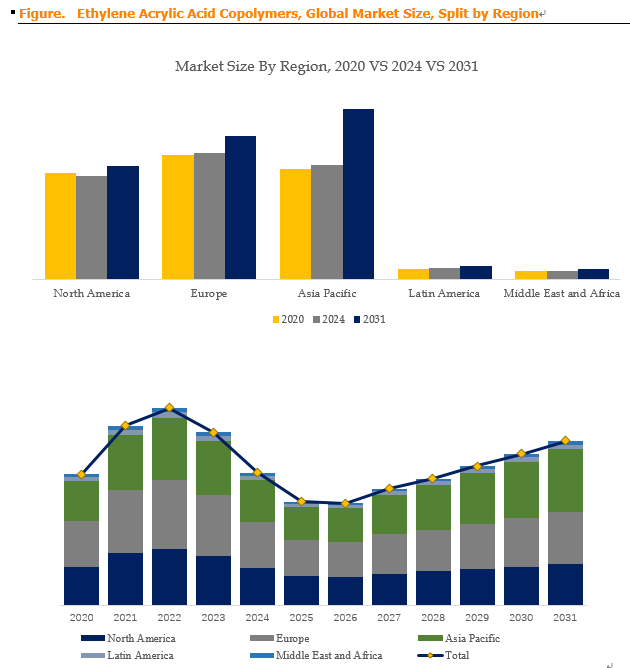

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by China's massive packaging industry (consumer goods, food, beverages), India's growing population and consumption, and Southeast Asia's manufacturing expansion. North America is a mature but significant market, driven by flexible packaging demand, food and beverage packaging, and automotive applications. Europe is a mature market with a strong focus on sustainable packaging and high-performance materials. The Middle East & Africa and Latin America are smaller but growing markets, driven by urbanization and industrial development.

0{Y.png)

Ethylene Acrylic Acid Copolymers Market Dynamics

Market Drivers:

-

D1: Growing demand for flexible packaging materials – Flexible packaging (pouches, bags, films, laminates) is growing at 4-6% annually, driven by:

-

Convenience and shelf appeal: Easy-to-open, re-sealable, and lightweight packaging.

-

Sustainability: Less material usage compared to rigid packaging.

-

Food safety and shelf life: Barrier films with high oxygen and moisture barriers.

-

Brand differentiation: High-quality graphics and visual appeal.

EAA is a key component in multi-layer flexible packaging as a tie layer (to bond incompatible polymers) and as a sealant layer (to provide strong, hermetic seals). As flexible packaging volume increases, so does EAA demand.

-

-

D2: Increased demand for high-barrier packaging in food and beverage – The push for longer shelf life, reduced food waste, and "clean label" products (without preservatives) drives demand for high-barrier packaging. Typical structures: PET/EVOH/PE, OPP/Aluminum/PE, Paper/Aluminum/PE, etc. EAA is critical as the tie layer between the polar barrier material (EVOH, aluminum, paper) and the non-polar sealing layer (PE, PP). Without EAA, these structures would delaminate.

-

D3: Growth of liquid packaging — cartons, pouches, and bags – Liquid packaging (milk, juice, water, soups, sauces, and liquid detergents) is transitioning from rigid containers (glass, HDPE bottles, cans) to flexible cartons, pouches, and bags. Paperboard-based liquid packaging (e.g., Tetra Pak, SIG, Elopak) uses EAA as a tie layer and sealant. Flexible pouches for liquid fillings also require EAA-based sealants.

-

D4: Replacement of conventional packaging materials with lightweight, functional alternatives – The shift from rigid packaging (glass, metal, rigid plastics) to flexible packaging reduces weight, shipping costs, and carbon footprint. EAA's compatibility with multi-layer structures enables this transition by providing strong adhesion and sealing.

-

D5: Expanding applications beyond packaging — adhesives, coatings, automotive – EAA is finding increasing use in:

-

Adhesives: Hot melt adhesives for bookbinding, packaging, and assembly.

-

Coatings: Paper coatings for grease resistance, metal coatings for corrosion protection.

-

Automotive: Underbody coatings, interior trim, and composite bonding.

-

Construction: Roofing membranes, sealants.

These new applications are driving EAA demand outside traditional packaging.

-

Market Restraints:

-

R1: High raw material cost and availability of acrylic acid – EAA production depends on ethylene (derived from naphtha or natural gas) and acrylic acid. Acrylic acid is a specialty chemical, and its production capacity is limited to a few global producers. Acrylic acid prices can be volatile (driven by supply-demand, propylene prices, and trade issues). High acrylic acid cost (relative to other comonomers) makes EAA more expensive than alternative materials (e.g., anhydride-modified polyolefins, EVA, ionomers).

-

R2: Competition from alternative materials – EAA faces competition from:

-

Anhydride-modified polyolefins (MAH-grafted PE/PP): Similar adhesion and sealing properties, often at lower cost. Used as tie layers and sealants.

-

Ethylene vinyl acetate (EVA): Lower cost, good sealing properties, but lower adhesion and thermal stability.

-

Polyurethane adhesives: Used in flexible packaging (solvent-based or solvent-free), offering good adhesion but with additional processing costs.

-

Ionomers (e.g., Surlyn®): Offer superior impact resistance and clarity but are more expensive.

-

PE/PP blends: Cheaper but less effective for adhesion to polar substrates.

As packaging manufacturers seek to reduce material costs, they may switch to alternative materials, limiting EAA market growth in cost-sensitive applications.

-

-

R3: Increasing focus on mono-material and recyclable packaging – The packaging industry is moving toward mono-material packaging structures (i.e., made from a single polymer family, such as all-PE or all-PP) to improve recyclability. Multi-layer structures with dissimilar materials (e.g., PET/PE, aluminum/PE, paper/PE) are increasingly scrutinized for recycling compatibility. EAA, as a multi-layer tie layer, could be impacted if packaging design shifts toward simpler, mono-material structures. Manufacturers are developing "recyclable-friendly" EAA grades or alternative tie layers that are compatible with mono-material recycling streams.

-

R4: Regulatory pressure on packaging materials – Food contact regulations (FDA in the US, EU FCM, China GB) require extensive compliance testing for EAA and its degradation products. Any new EAA grade or formulation must undergo extraction and migration testing. In addition, single-use plastics regulations and packaging waste directives (EU PPWD, China's bans) may reduce demand for certain packaging formats using EAA.

Market Opportunities:

-

O1: Development of bio-based EAA – There is growing demand for bio-based polymers from renewable feedstocks (bio-ethylene and bio-acrylic acid) to reduce carbon footprint and improve sustainability profile. Manufacturers developing bio-based EAA with comparable performance can capture premium pricing and gain a competitive advantage.

-

O2: Development of recyclable EAA grades – To address the mono-material trend, EAA manufacturers are developing "recyclable" grades that are compatible with PE recycling streams (i.e., not disrupting the recycling process). These grades may incorporate de-bondable layers, lower acid content, or compatibilizing technologies.

-

O3: Growth of paper-based packaging requiring EAA – With increasing bans and restrictions on single-use plastics, paper-based packaging (often with EAA coatings or laminations) is growing. EAA provides the required moisture and grease barrier while maintaining the "paper" aesthetic and recyclability (in some cases).

-

O4: Expansion into emerging markets (India, Southeast Asia, Middle East) – As consumer populations grow and packaging consumption rises, EAA demand in emerging markets increases. Establishing production, distribution, or technical service capabilities in these regions can capture market share.

-

O5: Innovations in high-performance EAA grades – Development of high-melt-strength EAA for blow molding, high-flow grades for injection molding, and high-adhesion grades for demanding applications (e.g., automotive, electronics) provides opportunities for product differentiation.

-

O6: EAA in electric vehicle (EV) battery applications – EAA and its ionomer derivatives are being explored for battery applications:

-

Binder for cathodes: EAA-based binders offer adhesion and flexibility for cathodes.

-

Encapsulation: EAA-based sealants for battery pack sealing.

-

Separator coatings: For improved thermal stability and shutdown performance.

While still in early stages, the EV market could become a significant new demand source for EAA.

-

Industry Structure and Competitive Dynamics

The global Ethylene Acrylic Acid Copolymers market is characterized by:

-

South Korean leader (SK Geo Centric): A major producer of EAA, with significant production capacity and a strong presence in the Asian market. SK Geo Centric has been investing in capacity expansion and R&D.

-

US leader (ExxonMobil Chemical): A major global player with significant capacity, broad product portfolio, and strong technical support. ExxonMobil offers a range of EAA grades (e.g., Escor™) and has a global supply chain.

-

Other players (Dow, LyondellBasell, regional producers): Dow and LyondellBasell offer EAA or ionomer products (Dow's Nucrel™ and Surlyn™). Regional producers (in China, Europe, or Middle East) are emerging to meet local demand.

Key success factors in this market:

-

Technology leadership: High-pressure polymerization technology, process control, and ability to produce a wide range of EAA grades.

-

Scale and cost competitiveness: Large-scale production reduces unit costs, enabling competitive pricing.

-

Product quality and consistency: Packaging manufacturers require tight specifications and batch-to-batch consistency.

-

Customer relationships and technical support: Close collaboration with packaging converters and brand owners to develop custom grades and solve application issues.

-

Regulatory compliance: Food contact compliance and environmental regulations require rigorous testing and documentation.