+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Zirconia Dispersion for OLED Market to Reach $0.12 Billion by 2031, Growing at 8.31% CAGR

Global Zirconia Dispersion for OLED Market to Reach $0.12 Billion by 2031, Growing at 8.31% CAGR

Friday,03 Jul,2026

Zirconia Dispersion for OLED: Definition and Principles

Zirconia dispersions are high-performance materials in which nano-sized zirconium oxide (ZrO₂) particles are stably dispersed in aqueous or organic solvents. Zirconia, which possesses a high refractive index (approximately 2.15–2.20, depending on crystal phase), excellent thermal stability (melting point ~2,700°C, capable of withstanding OLED processing temperatures), and high mechanical strength, is finely divided using specialized dispersion technology to achieve uniform particle distribution and high transparency (maintaining >90% transmittance in the visible spectrum).

In OLED (Organic Light Emitting Diode) applications, zirconia dispersion plays a valuable role due to its optical clarity, thermal stability, and electrical insulation properties. In OLED device fabrication, zirconia nanoparticles dispersed in solvents can be used to form thin, uniform layers that serve various functional purposes:

-

Encapsulation materials (primary application): The high refractive index and transparency of zirconia dispersions enhance light extraction efficiency — by reducing total internal reflection and improving out-coupling of light generated in the emissive layer, device brightness and energy efficiency are improved. Zirconia-based encapsulation layers also provide effective barrier properties against moisture and oxygen, which are detrimental to OLED longevity.

-

Barrier coatings: Zirconia layers act as diffusion barriers, preventing ingress of moisture and oxygen into the sensitive organic layers, thus significantly extending the operational lifespan of OLED panels.

-

Charge-blocking or diffusion layers: Zirconia-based layers can be engineered as electron-blocking or hole-blocking layers, optimizing current balance and improving charge injection efficiency, which enhances device performance and stability.

-

Refractive index matching layers: In OLED stack architectures, zirconia layers help to match refractive indices between adjacent layers, reducing optical losses and improving overall device efficiency.

62LT9DA9T.png)

Key advantages of zirconia dispersion over alternative materials:

| Property | Zirconia (ZrO₂) | Silica (SiO₂) | Titania (TiO₂) | Alumina (Al₂O₃) |

|---|---|---|---|---|

| Refractive Index | 2.15–2.20 | 1.45–1.46 | 2.5–2.7 | 1.76–1.78 |

| Thermal Stability | Excellent (Tm ~2700°C) | Good (Tm ~1710°C) | Good (Tm ~1840°C) | Excellent (Tm ~2070°C) |

| Chemical Inertness | Excellent | Excellent | Photocatalytic (degradation risk) | Good |

| Electrical Insulation | Excellent | Excellent | Semiconductor (TiO₂) | Good |

| Transparency (visible) | Excellent (>90%) | Excellent (>95%) | Good (slight yellow tint) | Good (>90%) |

Processing compatibility: Thanks to its nano-scale uniformity and chemical inertness, zirconia dispersion is compatible with solution-based processing technologies — such as inkjet printing, spin coating, slot-die coating, and spray coating — making it suitable for large-area OLED production and roll-to-roll manufacturing.

Zirconia Dispersion for OLED Market Summary

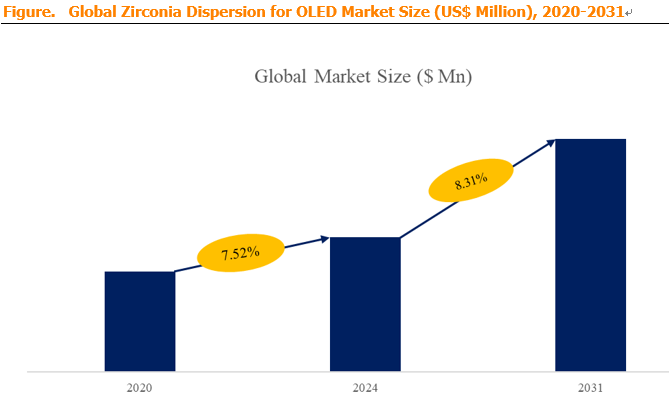

According to a new market research report published by Market Monitor Global, the global Zirconia Dispersion for OLED market is projected to reach USD 0.12 billion (approximately $120 million) by 2031, at a compound annual growth rate (CAGR) of 8.31% during the forecast period. This robust growth is driven by the expanding OLED display market (smartphones, TVs, wearables, AR/VR, automotive displays), the increasing penetration of high-refractive-index materials in encapsulation and optical enhancement layers, and the rising demand for improved light extraction efficiency and device longevity.

Market Monitor Global's analysis indicates that the global key manufacturers of Zirconia Dispersion for OLED include Nippon Shokubai (Japan) and DIC (Japan). In 2024, the global top three players collectively accounted for approximately 31.7% of total revenue, indicating a moderately concentrated market with a limited number of specialized suppliers. The market is characterized by high technical barriers (dispersion stability, particle size control, purity requirements), specialized manufacturing processes, and long qualification cycles (typically 12-24 months for OLED manufacturers to qualify a new zirconia dispersion supplier). While Japanese manufacturers dominate the premium segment, there is growing participation from Korean and Chinese specialty chemical companies, responding to the rapid expansion of the OLED display industry in Asia.

In terms of product type (by solvent system), the market is segmented into Aqueous-Based and Solvent-Based dispersions. Solvent-based dispersions (using organic solvents such as propylene glycol monomethyl ether acetate (PGMEA), butyl acetate, or cyclohexanone) are more commonly used in OLED processing, as they are compatible with the organic solvents used in photolithography and inkjet printing processes, and offer better film-forming properties and higher solids loading. Aqueous-based dispersions are gaining interest for environmentally friendly processes and certain niche applications where water-compatible materials are required.

Regarding application, Encapsulation is the largest segment, accounting for the majority of zirconia dispersion consumption in OLED manufacturing. Optical Enhancement Layers (light extraction, refractive index matching) and Barrier/Protective Layers are also significant. Other Applications (charge-blocking layers, diffusion layers, and emerging uses) account for the remainder.

Regional dynamics: Asia-Pacific is the dominant region, accounting for over 80% of the global market, driven by the concentration of OLED panel production in South Korea (Samsung Display, LG Display), China (BOE, Visionox, TCL CSOT, Tianma, Everdisplay), Japan (JOLED, though JOLED filed for bankruptcy in 2023, technology continues to influence the market), and Taiwan. China is the fastest-growing regional market, with rapid expansion of OLED fabs and growing domestic demand for high-performance display materials. South Korea and Japan remain significant markets due to their leadership in advanced OLED materials and technology. North America and Europe are smaller but important markets, driven by R&D activities, AR/VR development, and niche applications (automotive, aerospace).

Zirconia Dispersion for OLED Market Dynamics

Market Drivers:

-

D1: Proliferation of OLED displays across consumer electronics and automotive sectors – OLED displays have become the dominant technology in high-end smartphones, are increasingly adopted in TVs (with LG and Samsung leading the market), and are growing in wearables (smartwatches, fitness trackers), tablets, and laptops. Automotive OLED displays (instrument clusters, center consoles, side-view mirrors, rear-seat entertainment) are gaining traction, with high durability and aesthetic design requirements. As OLED panel production capacity expands (particularly in China), demand for high-performance materials — including zirconia dispersion — grows.

-

D2: Rising demand for high-refractive-index and thermally stable materials in OLED encapsulation – OLED devices are highly sensitive to moisture and oxygen, requiring encapsulation layers with excellent barrier properties. Zirconia-based encapsulation films offer both high refractive index (improving light out-coupling) and robust barrier performance, enhancing both efficiency and device lifetime. As OLED panel manufacturers push for higher brightness, lower power consumption, and longer lifetimes, zirconia dispersion's value proposition strengthens.

-

D3: Growing demand for light extraction efficiency improvement – A significant portion of light generated in OLED devices is trapped due to total internal reflection, reducing external quantum efficiency (EQE). High-refractive-index layers (such as zirconia-based coatings) help to extract more light by reducing the refractive index mismatch between the OLED stack and the air/glass interface. As OLED manufacturers seek to improve efficiency without increasing power consumption (critical for portable devices), demand for high-refractive-index optical enhancement layers increases.

-

D4: Expansion of inkjet-printed and solution-processed OLED manufacturing – While vacuum-deposited small-molecule OLEDs dominate the premium smartphone and TV markets, solution-processed OLEDs (using inkjet printing, slot-die coating, or spin coating) are gaining traction for large-area displays (TVs, signage) and flexible/rollable displays. Zirconia dispersions are compatible with these solution-based processes, enabling low-cost, high-throughput manufacturing for large-format panels. This compatibility opens up new market opportunities for zirconia dispersion beyond the premium, small-molecule segment.

-

D5: Emergence of AR/VR and XR devices requiring high-performance optics – Augmented reality (AR), virtual reality (VR), and mixed reality (XR) devices require advanced optical components — including high-refractive-index films, lenses, and waveguides — to achieve wide field-of-view, high resolution, and low optical aberrations. Zirconia dispersions are increasingly used in these optical components due to their high refractive index, transparency, and compatibility with advanced manufacturing processes (nanoimprint lithography, micro-optics fabrication). As the metaverse and XR hardware market accelerates (headsets from Meta, Apple Vision Pro, Sony, HTC, etc.), zirconia dispersion demand from the optics sector increases.

Market Restraints:

-

R1: High technical barriers — precise particle size control, dispersion stability, and batch-to-batch consistency – High-performance zirconia dispersions require precise control over:

-

Particle size and distribution: Typically <50 nm, with narrow distribution (monodisperse), to achieve high transparency and prevent scattering.

-

Surface chemistry: The particle surface must be modified (e.g., with silane coupling agents, organic acids, or polymeric dispersants) to achieve stable dispersion in the chosen solvent system and prevent agglomeration.

-

Dispersion equipment: High-energy bead mills, ultrasonic dispersers, or high-shear mixers, with controlled energy input to avoid particle breakage or contamination.

-

Purity: Trace metal impurities (Fe, Cu, Na, K, Ca, etc.) must be <1 ppm to avoid electrical defects or quenching of OLED emission.

Achieving and maintaining these requirements during scale-up to industrial production volumes is difficult. Small-to-medium companies often struggle to justify the capital investment and technical expertise required.

-

-

R2: Limited supplier base and long qualification cycles – OLED panel manufacturers require rigorous qualification of new zirconia dispersion suppliers, including:

-

Material characterization: Particle size, distribution, stability, purity, solids content, viscosity, pH/conductivity, and compatibility with OLED materials.

-

Device testing: Performance in actual OLED devices (efficiency, lifetime, brightness, color, electrical characteristics).

-

Long-term stability: Monitoring dispersion stability over time (shelf life) and performance over extended device operation.

Qualification cycles typically take 12-24 months. Once qualified, suppliers are rarely changed — creating high barriers to entry and limited competition.

-

-

R3: Competition from alternative materials – While zirconia offers excellent properties, alternative high-refractive-index materials are being developed:

-

Titania (TiO₂) dispersions: Higher refractive index (~2.5-2.7) than zirconia, but TiO₂ has photocatalytic activity (degradation risk) and can cause yellow tint, limiting its use in transparent optical layers.

-

Alumina (Al₂O₃) dispersions: Lower refractive index (~1.76-1.78) than zirconia, but higher thermal stability and lower cost for some applications.

-

Hybrid organic-inorganic materials: Silica-nanoparticle loaded polymers, or organic polymers with high refractive index (e.g., polyimides, polythioureas), which may offer lower cost or easier processing.

-

Quantum dots and perovskite materials: Emerging display technologies that may reduce or eliminate the need for certain optical layers.

Competition from these alternatives limits the market share growth of zirconia dispersion, particularly in cost-sensitive applications.

-

-

R4: Raw material price volatility and supply chain risks – Zirconium-based raw materials (zirconium oxychloride, zirconium isopropoxide, etc.) are subject to supply-demand fluctuations and geopolitical factors (China is a major producer of zirconium chemicals). Volatility in raw material prices affects production costs and pricing stability for zirconia dispersion manufacturers.

Market Opportunities:

-

O1: Expansion of zirconia use in OLED encapsulation beyond current levels – As OLED panel manufacturers push for longer lifetimes (particularly for automotive, signage, and large-area displays), the demand for high-performance encapsulation materials — including zirconia-based barrier layers — will increase. Manufacturers that can offer higher-performance zirconia dispersions (e.g., higher refractive index, better barrier performance, improved process compatibility) will capture premium pricing and secure long-term supply agreements.

-

O2: Development of high-refractive-index zirconia dispersions for AR/VR optics – AR/VR devices require optical components with high refractive index (>1.7) to achieve compact optical designs (thin, lightweight) while maintaining high image quality and wide field-of-view. Zirconia dispersions (nanoparticle-loaded photoresists, imprint resins, or optical coatings) are key enablers for micro-optics, waveguides, and diffractive optical elements. As the AR/VR market grows (projected to exceed $100 billion by 2030), demand for high-refractive-index materials — including zirconia — will increase.

-

O3: Eco-friendly, aqueous-based zirconia dispersions for sustainable manufacturing – With increasing environmental regulations and corporate ESG commitments, there is growing interest in water-based, non-toxic, and low-VOC (volatile organic compound) formulations. Aqueous-based zirconia dispersions (using water as solvent) offer environmental advantages over organic solvent systems. While aqueous systems may have challenges (drying time, compatibility with hydrophobic OLED materials), manufacturers that develop robust, high-performance aqueous dispersions can differentiate themselves in the sustainability-conscious market.

-

O4: Customization for specific OLED architectures – OLED device architectures vary: top-emission vs. bottom-emission, flexible vs. rigid, large-area vs. small-area, and different emissive materials (fluorescent, phosphorescent, TADF). Each architecture may require specific optical, barrier, or electrical properties from zirconia layers. Manufacturers that can offer customized zirconia dispersions — tailored to specific OLED designs, solvent systems, and process conditions — can build stronger, more defensible customer relationships.

-

O5: Integration with nanoparticle-based functional layers – Beyond standalone zirconia layers, manufacturers can develop multi-functional nanoparticle dispersions — for example, zirconia combined with other functional nanoparticles (titania, silica, or phosphors) to achieve combined optical and barrier effects. These composite dispersions can simplify OLED device processing (reducing the number of layers) and offer differentiated performance.

-

O6: Expansion into other display technologies (microLED, QD-OLED) – While OLED is the immediate application, zirconia dispersions may also find applications in emerging display technologies:

-

MicroLED: Requires high-refractive-index encapsulation and optical coupling layers, similar to OLED.

-

QD-OLED (Quantum Dot OLED): Hybrid display technology combining OLED emission with quantum dot color conversion; zirconia layers may be used in optical enhancement and encapsulation.

Manufacturers that adapt zirconia dispersions for these emerging display technologies can diversify their customer base and reduce reliance on the OLED market.

-

Industry Structure and Competitive Dynamics

The global Zirconia Dispersion for OLED market is characterized by:

-

Japanese leaders (Nippon Shokubai, DIC): These companies have long histories in specialty chemicals, dispersion technology, and OLED materials. They have deep expertise in particle synthesis, surface chemistry, dispersion formulation, and OLED device qualification. They maintain strong relationships with major OLED panel manufacturers (Samsung Display, LG Display, BOE) and command premium pricing for high-performance products.

-

Korean and Chinese emerging players: Specialty chemical companies in Korea and China are developing zirconia dispersion capabilities, leveraging the rapid growth of domestic OLED production. These include companies with expertise in ceramics, nanomaterials, and display materials. They are gaining share in mid-tier applications and cost-sensitive segments.

-

Niche players: Smaller companies focusing on specific applications (e.g., AR/VR optics, flexible displays, or aqueous dispersions) with differentiated products.

Key success factors in this market:

-

Particle technology expertise: Synthesis of monodisperse, high-purity, non-agglomerated nanoparticles.

-

Dispersion stability: Ability to maintain stable, uniform dispersion over extended shelf life and during processing (shipping, storage, coating, baking).

-

Device performance: Demonstrated improvements in OLED efficiency, brightness, lifetime, and color purity in actual OLED devices.

-

Process compatibility: Compatibility with OLED manufacturing processes (inkjet printing, spin coating, vacuum deposition, photolithography).

-

Customer relationships and qualification: Strong relationships with OLED panel manufacturers and ability to navigate the long, rigorous qualification process.

-

Cost competitiveness: Effective management of raw material costs, manufacturing yields, and scaling.